How to Stop Living Paycheck to Paycheck: A Step-by-Step Plan for 2026

How to Stop Living Paycheck to Paycheck, Starting This Month

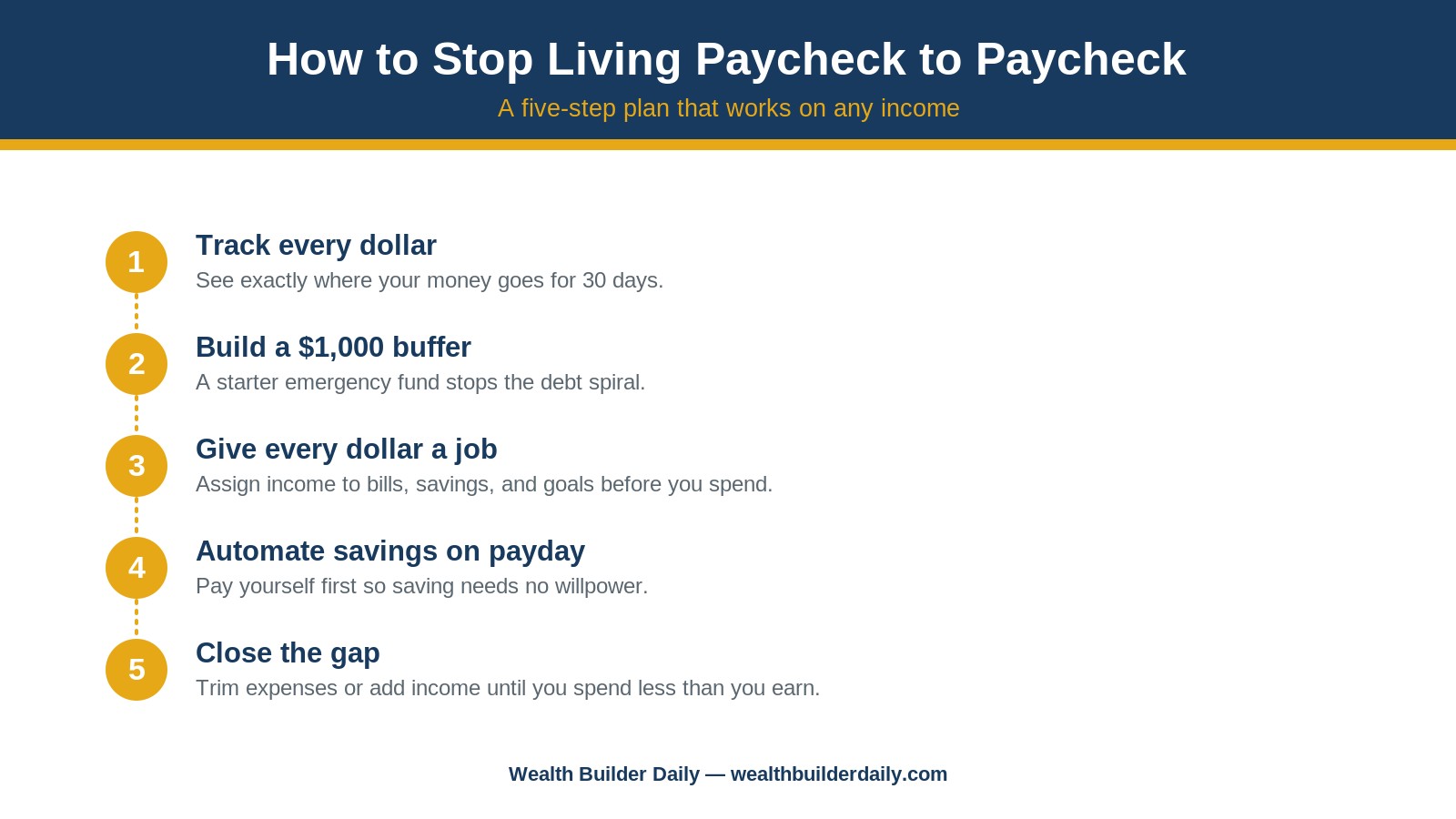

To stop living paycheck to paycheck, you need to do three things in order: see exactly where your money goes, build a small cash buffer, and give every future dollar a job before it lands in your account. That is the whole plan in one sentence, and it works whether you earn $2,800 a month or $8,000.

This guide is for anyone who feels like the money disappears the moment it arrives. Maybe you have a decent income but nothing to show for it, or maybe a single surprise bill sends you straight to a credit card. We will walk through why the cycle happens, the exact five steps to break it, and how to choose the right first move for your situation in 2026.

Breaking the Paycheck-to-Paycheck Cycle at a Glance

The cycle is not really about how much you make. It is about the gap between what comes in and what goes out, and whether you have a system for the space in between. Here is the quick version before we dig in.

| Question | Short Answer | |---|---| | What does "paycheck to paycheck" mean? | You spend nearly all your income before the next payday, leaving little or nothing to save. | | What is the very first step? | Track every dollar for 30 days so you can see where your money actually goes. | | How big should my starter buffer be? | A $1,000 cash buffer stops most small emergencies from becoming new debt. | | How long until I feel relief? | Most people feel real breathing room within 60 to 90 days of following a written plan. | | Do I need a high income to do this? | No. The plan works on any income because it targets the gap, not the paycheck. |

A few facts worth holding onto as you read:

- A written spending plan matters more than income level. The Consumer Financial Protection Bureau consistently finds that people who follow a written budget are far more likely to hit savings goals.

- The fastest wins come from a starter emergency fund, not from waiting for a bigger paycheck.

- Heading into 2026, a large share of American households across every income bracket still report living paycheck to paycheck, so you are not an outlier.

- Automating your savings removes willpower from the equation, which is the single biggest reason plans fail.

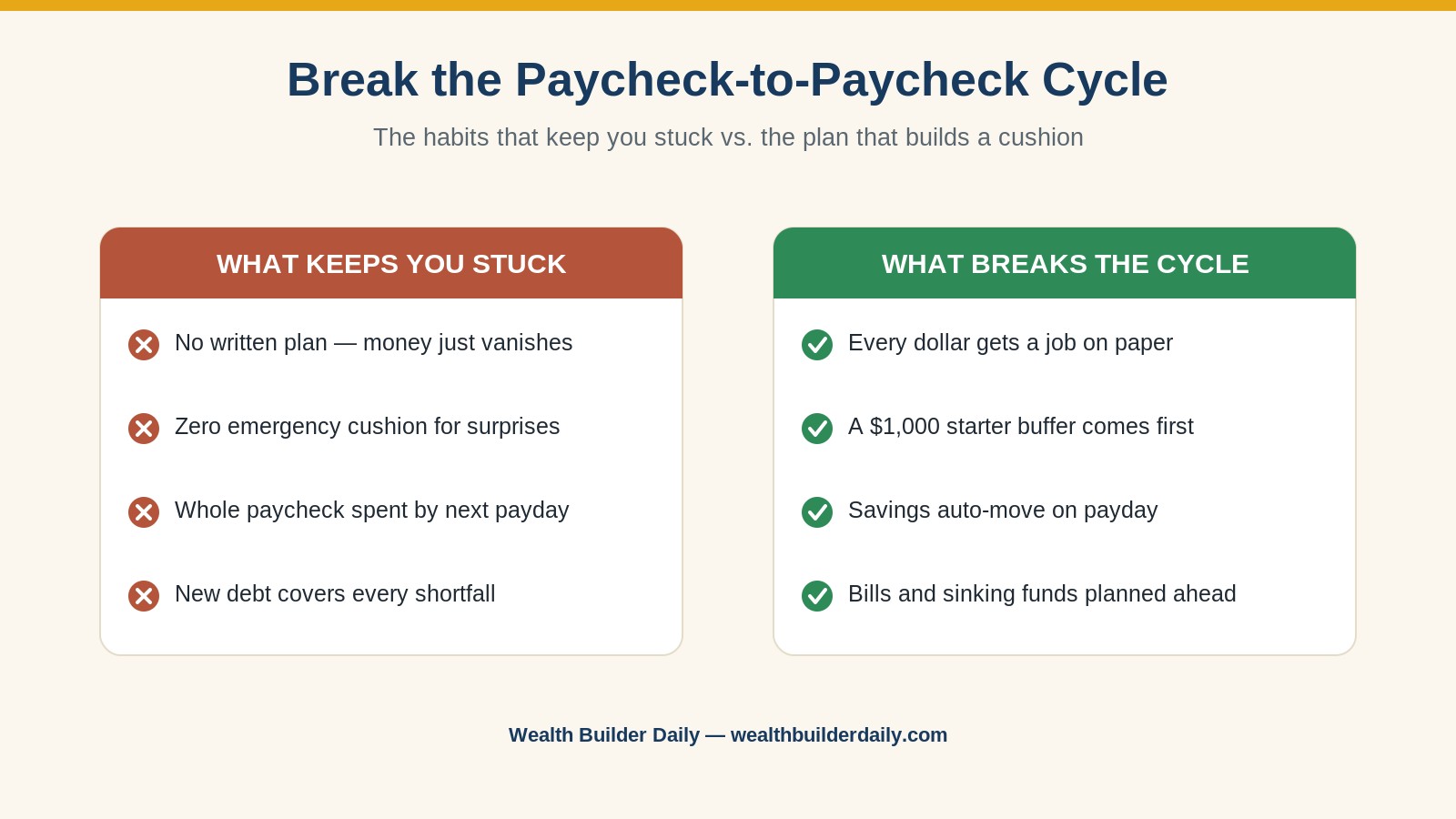

Why Most People Stay Stuck

At Wealth Builder Daily, we have spent years helping everyday earners get off the paycheck-to-paycheck treadmill, and the pattern is almost always the same. It is rarely a spending problem in the way people think. It is a visibility problem. Money leaves in dozens of small, forgettable transactions, so at the end of the month there is nothing left and no clear story of where it went. When a surprise cost lands, there is no cushion, so a credit card fills the gap. Next month, the minimum payment on that card makes the shortfall a little worse. That is the trap: not overspending on big luxuries, but drifting without a plan while small leaks and new debt quietly close the door on saving.

The good news is that the fix is mechanical, not magical. Once you make your money visible and put a system around it, the cycle loses its grip surprisingly fast.

How Breaking the Paycheck-to-Paycheck Cycle Works

Breaking the paycheck-to-paycheck cycle works by replacing guesswork with a repeatable five-step routine. Each step removes one of the reasons the cycle survives: no visibility, no buffer, no plan, no automation, and no margin. Here is what each step does.

- Track every dollar (30 days): You cannot fix a leak you cannot see. Writing down every purchase for a month turns a vague feeling into hard numbers.

- Build a $1,000 buffer: This starter cushion is what stops a flat tire or a copay from becoming credit card debt. It is the circuit breaker for the whole cycle.

- Give every dollar a job: Before payday, you assign your income to bills, savings, and goals so there is nothing left to "accidentally" spend.

- Automate savings on payday: A recurring transfer moves money to savings before you can touch it, so progress does not depend on discipline.

- Close the gap: You trim expenses, raise income, or both, until you reliably spend less than you earn month after month.

The order matters. Trying to automate savings before you have visibility or a buffer usually backfires, because the first emergency drains the account and you give up. Follow the steps in sequence and each one makes the next easier.

How to Choose the Right First Move

You do not have to do all five steps at once. Pick the one that fixes your biggest weakness first, then build from there. Use these criteria to decide.

- Start with your biggest leak. After a week of tracking, one or two categories almost always jump out: dining out, subscriptions, rideshares, or impulse online orders. Cut the largest one first for the fastest visible win.

- Choose a method you will actually stick with. A plan you abandon in two weeks helps no one. If you like structure, try a zero-based budget. If you want something lighter, the 50/30/20 rule is easier to maintain.

- Automate the first $50. Do not wait until you can save a lot. A small automatic transfer builds the habit and the buffer at the same time. You can raise it later.

- Attack one debt at a time. Spreading extra money across five balances feels productive but moves slowly. Put your extra dollars on the smallest balance while paying minimums on the rest.

- Give irregular costs a home. Car repairs, insurance, and holidays are not emergencies; they are predictable. Set up sinking funds so these do not blow up your month.

- Set a 15-minute weekly check-in. A short, recurring money review keeps small problems from snowballing and keeps the plan alive.

Here is the expert tip most people skip: automate your savings for the day after payday, not the day before your next one. Even $75 per paycheck, moved automatically twice a month, quietly builds $1,800 over a year without a single act of willpower. Pairing that with a pay-yourself-first system is the closest thing to a shortcut that exists.

Buffer Fund vs. Full Emergency Fund

These are not the same thing, and confusing them stalls a lot of people. A buffer fund is a small $1,000 starter cushion you build first, fast, to stop new debt. A full emergency fund is three to six months of expenses that you build later, more slowly, for job loss or major events. Build the buffer now. Build the full fund after your gap is closed and your debt is under control.

A Plan for Every Situation

There is no single "right" version of this plan. The steps stay the same, but the emphasis shifts depending on your life.

- Single earner on a tight budget: Your leverage is on the expense side. Focus hard on the $1,000 buffer and cutting your two largest discretionary categories before worrying about investing.

- Two-income household with lifestyle creep: Your income is fine; your spending grew with it. Run every subscription and recurring charge through a single review, and automate savings so the extra income builds wealth instead of habits.

- Variable or irregular income: Base your plan on your lowest recent month, not your best one. Our guide to budgeting on irregular income shows how to smooth out the highs and lows so you stop feeling whiplash.

Beginner, Intermediate, and Advanced Setups

If you are just starting, keep it to two moves: track for 30 days and open a separate savings account for your buffer. At the intermediate stage, add a written monthly plan and one automatic transfer per paycheck. At the advanced stage, layer in sinking funds for every predictable expense, a full emergency fund, and automated investing once your gap is reliably positive.

Personalizing Your Plan in 2026

The tools have never been better. In 2026, most banks let you open multiple free savings accounts and nickname them, so you can hold your buffer, your car fund, and your holiday fund in separate labeled buckets. Set your automatic transfers to hit the day after each payday, review your plan for 15 minutes every weekend, and adjust the numbers as your income and costs change. Personalization is not about a fancy app; it is about matching the plan to your real paydays and your real bills.

Frequently Asked Questions

How do I stop living paycheck to paycheck on a low income?

Start with visibility and a tiny buffer rather than big cuts. Track every dollar for 30 days to find your largest leak, then automate even $25 per paycheck into a separate account. On a low income, closing the gap often means adding a small side income alongside trimming expenses, so treat both sides of the equation as fair game.

How long does it take to break the paycheck-to-paycheck cycle?

Most people feel meaningful relief within 60 to 90 days once they follow a written plan and build a $1,000 buffer. Fully closing the gap, paying down the debt that fed the cycle, and building a real emergency fund usually takes six to twelve months. The early breathing room comes fast, which is what keeps you going through the longer work.

Should I pay off debt or save first?

Do both in a specific order. Build a small $1,000 buffer first so new emergencies stop creating new debt, then throw extra money at your highest-interest balance. Once that debt is gone, redirect those same payments into a full emergency fund and investing. The buffer comes first because without it, one bad month undoes months of debt payoff.

Final Thoughts

You do not need a bigger paycheck to stop living paycheck to paycheck. You need visibility, a small buffer, a plan for every dollar, and a little automation, applied in that order. Start with 30 days of tracking and your first automatic transfer this week, and you will likely feel the difference before 2026's next season rolls around.

Here is why the Wealth Builder Daily approach works when others fizzle out:

- Plain-language guidance: No jargon and no shame, just clear steps you can act on today.

- Real numbers and examples: Every tip is anchored to actual dollar figures, not vague advice.

- Proven, time-tested methods: Track, buffer, budget, automate, and close the gap are the same fundamentals financial coaches have used for decades.

- Free practical tools and guides: Our library of budgeting and saving walkthroughs is free and built for everyday earners.

Your next payday is the perfect place to start. Pick one step, set up one automatic transfer, and let momentum do the rest, then keep going with more free guides on the Wealth Builder Daily blog. For a trustworthy, unbiased primer on budgeting and saving basics, the government's Consumer Financial Protection Bureau offers free tools worth bookmarking. The cycle ends the moment you decide to give your money a plan.

The Newsletter

Get the Free Budget Tracker

Join our weekly newsletter. Practical money guides, no fluff. Unsubscribe anytime.