Budgeting for Couples: How to Manage Money Together Without Fighting in 2026

Budgeting for couples works best when you combine your incomes, agree on shared goals, and split expenses fairly — so money becomes a team project instead of a recurring fight. If you and your partner keep bumping into the same money tension, the problem usually isn't how much you earn. It's that you never built a clear system you both understand.

This guide is for couples at any stage — dating and merging finances for the first time, newly married, or years in and ready for a reset. You'll get a plain-language system, a fair way to split bills, the exact accounts to set up, and a simple monthly habit that keeps you on the same page heading into 2026.

Budgeting for Couples at a Glance

The fastest way to stop money fights is to pick a clear structure for your accounts. There's no single right answer — the best system is the one you'll both actually use. Here's how the three most common approaches compare.

| Money System | Best For | How It Works | Watch Out For | |---|---|---|---| | Fully Joint | Couples who share most goals and income | All income and bills flow through shared accounts | Less personal privacy; needs high trust | | Fully Separate | New couples or large income gaps | Each keeps their own accounts and splits the bills | Easy to drift away from shared goals | | Yours, Mine, Ours | Most couples in 2026 | Joint account for shared bills, plus personal accounts | Takes a little setup and a monthly check-in |

A few quick facts to anchor your plan:

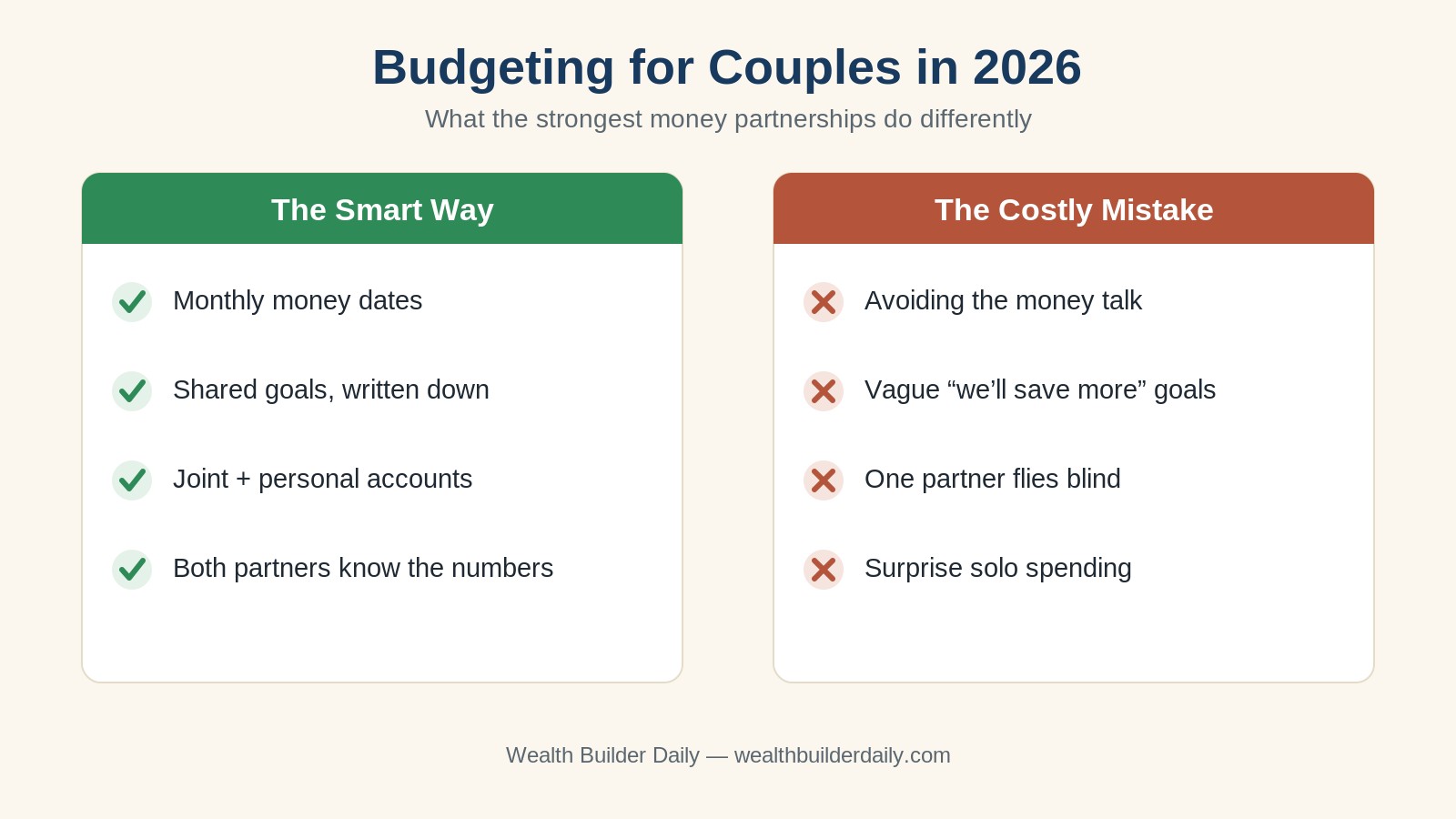

- Roughly 2 in 5 couples argue about money at least once a month, and an unclear system is usually the real cause — not the dollar amounts.

- A fair split is based on each person's share of income, not an automatic 50/50.

- Pairing your plan with the 50/30/20 budget rule gives you simple target percentages for needs, wants, and savings.

- Automating shared savings beats relying on willpower every single time.

Why Budgeting for Couples Beats Going Solo

At Wealth Builder Daily, we've spent years helping everyday people turn messy finances into calm, repeatable systems — and couples are where a good system pays off the most. Two people pulling in the same direction can save faster, pay off debt sooner, and weather emergencies far better than two people quietly managing money in separate corners. When you budget as a team, every extra dollar has a name and a job — and that, far more than a big salary, is how ordinary households build real wealth over time. In this guide, we'll walk you through the exact structure, the fair-split math, and the monthly habit that keeps both partners informed and on board.

The difference between couples who feel calm about money and couples who feel anxious almost always comes down to the habits above. The good news: every habit on the left is something you can set up in an afternoon.

How Budgeting for Couples Works

Budgeting for couples comes down to four moving parts. Once these are in place, the system mostly runs itself, and your monthly check-in becomes a quick review instead of a tense negotiation.

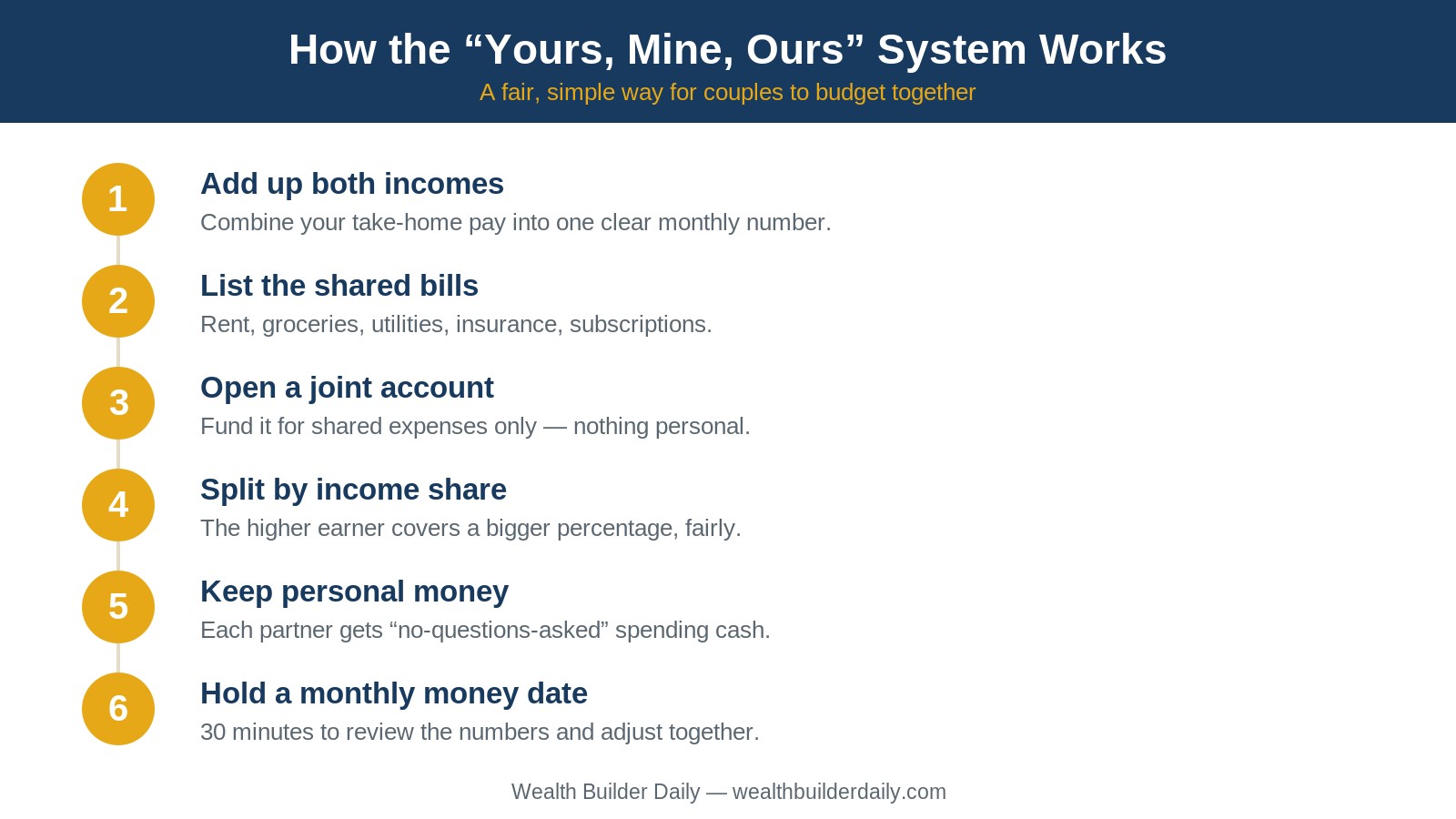

- One shared number. Add both take-home paychecks into a single combined monthly figure. This is the money your household actually has to work with.

- A clear expense split. Sort spending into shared (rent, groceries, utilities, insurance) and personal (hobbies, clothes, treats). Shared bills get funded together; personal money stays personal.

- A funding rule. Decide who contributes what to the joint account. Most couples find an income-based percentage feels fairest.

- A regular review. A short monthly money date keeps both partners aware of where things stand and catches small problems before they grow.

The most popular structure in 2026 is the "Yours, Mine, Ours" system, because it balances teamwork with independence. You fund shared goals together while each keeping a pool of no-questions-asked spending money. Here's the step-by-step.

Once the joint account is funded and your contributions are automated, your bills get paid without anyone having to "remember" whose turn it is. That alone removes one of the most common sources of money friction.

How to Choose the Right Money System for Your Relationship

There's no universal winner between joint, separate, and hybrid. Use these criteria to choose the setup that fits your relationship right now — and remember you can always adjust it later.

- Your income gap. If one of you earns much more, a percentage-based split usually feels fairer than a flat 50/50. A hybrid system handles this cleanly.

- Your trust and history. Fully joint accounts ask for the most transparency. If you're early in the relationship or rebuilding trust, start hybrid and merge more over time.

- Your shared goals. The bigger your shared dreams — a house, a wedding, kids, travel — the more a joint account helps you visibly pool money toward them.

- Your need for independence. If gifts, hobbies, or simply not being questioned about a coffee matter to you, build in personal accounts from day one.

- Your day-to-day money styles. A natural spender and a natural saver can absolutely thrive together, but they need a structure that protects shared savings from impulse buys.

Here's an expert tip with real numbers: if you and your partner each automate just $250 a month into a shared high-yield savings account earning around 4%, you'll have over $6,100 in two years, including a few hundred dollars in interest you didn't have to lift a finger for. Park that money in one of the best high-yield savings accounts so your shared goals grow while you sleep.

Joint vs. Separate Accounts: What Actually Works

Fully separate accounts feel safe, but they quietly make shared goals harder, because neither partner ever sees the full picture. Fully joint accounts build the strongest team mindset, but they can feel suffocating if one person likes a little financial privacy. For most couples, the hybrid "Yours, Mine, Ours" setup wins: a joint account for shared bills and savings, plus a personal account each. You get teamwork on the big stuff and freedom on the small stuff.

Budgeting for Couples in Every Situation

No two relationships have identical finances, so the system should flex to fit your life. Use the photo below as your reminder of the goal: a calm, organized household where money is handled, not feared.

Here's how the approach adapts to three common situations:

- Dual income, similar earnings. Split shared bills close to 50/50 and pour the rest into joint goals. This is the simplest setup, and a great time to build a shared emergency fund before anything else.

- One partner earns much more. Split shared bills by income percentage so the lower earner isn't stretched thin. The higher earner covers a bigger share, and both still keep personal money.

- Blended family or second marriage. Keep more separate at first, fund a joint account only for shared household costs, and revisit the split as trust and routines settle in.

Beginner, Intermediate, and Advanced Setups

A beginner couple might simply open one joint account for rent and groceries and automate equal transfers into it. An intermediate couple adds income-based contributions, a shared savings goal, and sinking funds for big yearly expenses like insurance and holidays. An advanced couple coordinates retirement contributions, decides together whether to pay off debt or invest first, and tracks a combined net worth.

Personalizing Your Plan in 2026

The tools have never been easier. In 2026, most couples can connect both partners to one of the best budgeting apps so the whole household budget updates in real time on both phones. Set shared goals inside the app, turn on automatic transfers on payday, and let the monthly money date become a five-minute review instead of an hour-long debate. Small, automated, and shared is the exact combination that quietly compounds into a stronger financial future for both of you.

Frequently Asked Questions

Should couples combine all their money?

Not necessarily. Fully combining works well for couples with shared goals and high trust, but plenty of strong couples thrive with a hybrid setup. The key is that shared bills and shared goals are funded together and both partners can see the full picture. Total privacy about money is usually what creates problems, not separate accounts themselves.

How do you split bills when one person earns more?

The fairest method is splitting by income share rather than 50/50. Add both incomes, find each person's percentage of the total, and have each partner cover that same percentage of shared bills. If one of you earns 60% of the household income, you cover 60% of the joint expenses. This keeps the lower earner from being stretched while the system stays balanced.

What is a money date and how often should we have one?

A money date is a short, scheduled check-in where you review your budget, savings progress, and any upcoming big expenses together. Once a month is plenty for most couples. Keep it to about 30 minutes, make it low-pressure, and pair it with coffee or a meal. The goal is shared awareness and small course corrections, not blame.

Final Thoughts

Budgeting for couples isn't really about spreadsheets — it's about turning money from a source of stress into a shared project you tackle as a team. Combine your income into one clear number, split the shared bills fairly, keep a little personal freedom, and protect it all with a quick monthly check-in. Do that, and the fights tend to fade while your savings quietly grow.

Here's why thousands of readers trust Wealth Builder Daily to guide their money decisions:

- Plain-language guidance. We explain every step in everyday words, so you never need a finance degree to follow along.

- Real numbers and examples. Our advice is grounded in actual dollar figures you can apply to your own household today.

- Proven, time-tested methods. We focus on systems that have helped real couples build wealth, not hype or get-rich-quick gimmicks.

- Free, practical tools and guides. Every resource we share is built to help you take action right now, at no cost.

Your next step is simple: pick your money system together this week, open or label your shared account, and schedule your first money date. For more free guides to help you and your partner build a stronger 2026, explore the rest of the Wealth Builder Daily blog, and for trustworthy, unbiased basics on managing money as a household, the Consumer Financial Protection Bureau is an excellent place to keep learning.

The Newsletter

Get the Free Budget Tracker

Join our weekly newsletter. Practical money guides, no fluff. Unsubscribe anytime.