No-Spend Challenge: How to Reset Your Budget and Save Fast in 2026

A no-spend challenge is a short, set period - usually 7, 14, or 30 days - where you pause every non-essential purchase and pay only for true needs, so you can save money fast and reset your spending habits. If your budget feels leaky and you want a quick win, a no-spend challenge is one of the simplest resets you can run in 2026.

This guide is for everyday earners who feel like money slips away on small, forgettable purchases. We'll cover exactly how a no-spend challenge works, how to set your rules, how to choose the right version for your life, and how to turn the money you save into lasting progress.

No-Spend Challenge at a Glance

Here's the short version: you decide what counts as "essential," draw a hard line around everything else, pick a time window, and stop spending on the non-essentials until the window closes. The money you would have spent stays in your account, and your only job is to move it somewhere it can grow.

| Question | Short Answer | |---|---| | What is it? | A set window where you spend only on true needs and pause everything else | | Who is it best for? | Impulse spenders, anyone in a rut, and savers who want a fast win | | What does it cost? | Nothing - it's designed to keep money in your pocket | | How long should it last? | Start with 7 to 30 days; many people repeat it monthly | | What's the catch? | You have to define "essential" honestly and plan ahead |

A few quick facts before we dig in:

- A no-spend challenge targets discretionary spending like takeout, impulse buys, and forgotten subscriptions - not rent, utilities, or basic groceries.

- You set the rules, so two people can run very different challenges and both succeed.

- The savings only count if you move the money out of checking - pair it with a high-yield savings account.

- It works as a one-time reset or a recurring habit you run every month in 2026.

A Quick Word on Where This Fits

At Wealth Builder Daily, we've spent years helping everyday people turn small habit changes into real savings, and the no-spend challenge is one of the first resets we recommend when a budget feels stuck. In this guide, we'll walk you through how to run a challenge that actually sticks - not a punishing month of deprivation, but a focused window that resets your defaults and shows you exactly where your money was leaking.

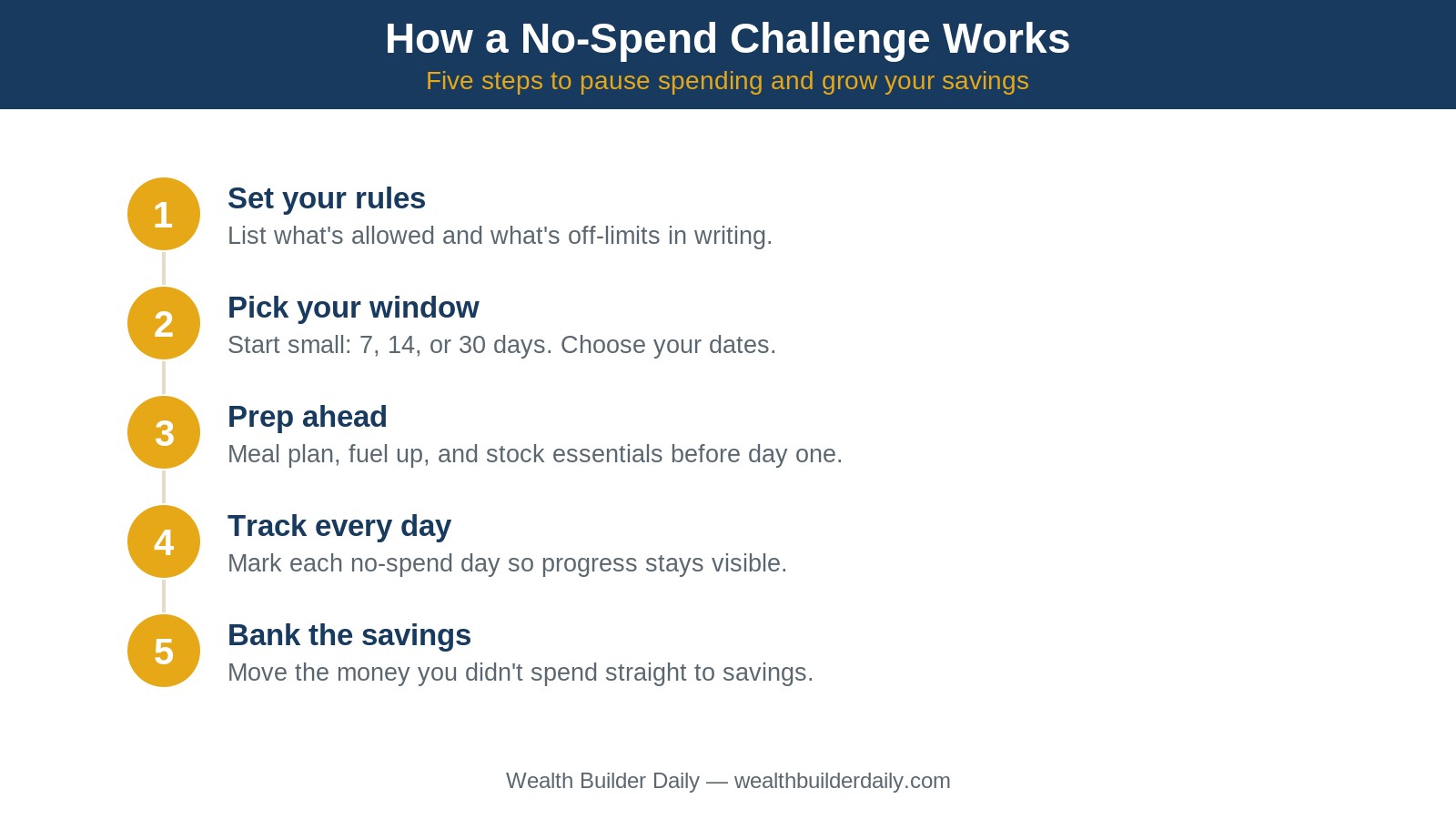

How a No-Spend Challenge Works

The no-spend challenge works by replacing dozens of small, automatic spending decisions with one big decision you make up front. Instead of asking "Should I buy this?" twenty times a day, you ask it once - before the challenge starts - and then you simply follow your own rule. That single shift removes the willpower drain that wrecks most budgets.

The effect is behavioral, not mathematical. Most overspending isn't dramatic. It's a $6 coffee here, a $14 lunch there, a $30 "treat yourself" purchase you forget by the weekend. None of it feels like much in the moment, but added together it's often hundreds of dollars a month. A no-spend challenge makes that invisible spending visible by forcing every non-essential purchase to bump into a rule you already set.

Here are the key parts that make a challenge work:

- A clear rulebook. You write down what's allowed and what's off-limits before day one, so there's no debating in the moment.

- A defined window. A fixed start and end date give you a finish line, which makes the challenge feel doable instead of endless.

- An honest essentials list. Rent, utilities, gas, insurance, medicine, and basic groceries stay in. Wants stay out.

- A savings destination. The money you don't spend has to go somewhere on purpose, or it quietly gets re-spent.

- A tracking method. A wall calendar, a notes app, or a simple checklist keeps each no-spend day in front of you.

How to Choose the Right No-Spend Challenge

There's no single "correct" no-spend challenge - the best one is the version you'll actually finish. Use these criteria to design yours.

-

Length. Pick a window that stretches you without breaking you. If you've never done this, start with 7 days. If you've got momentum, run a full no-spend month. Longer isn't better if it sets you up to quit on day four.

-

Strictness. Decide how hard the line is. A "soft" challenge might still allow one planned coffee out per week. A "strict" challenge allows zero discretionary spending. Both work - just choose on purpose instead of drifting.

-

Your essentials list. Be specific. Does "groceries" mean a full cart or just the basics you need to get through the week? Writing it down stops you from rationalizing a $90 grocery run that's really half snacks and convenience food.

-

Your spending triggers. Name the two or three places your money usually leaks - food delivery apps, late-night online shopping, the checkout line at Target - and plan around them. Delete the app, unsave the card, or pre-pack the meal.

-

Your savings target. Set a number. "I want to bank $400 this month" beats "I want to save more," because you can see whether you hit it.

Here's an expert tip with real numbers: even a modest challenge moves the needle. If you normally spend $12 a day on small extras and you run a strict 30-day no-spend challenge, that's roughly $360 you keep. Send that to a high-yield savings account earning around 4% in 2026, repeat it a few times a year, and you've built a real cushion from money that used to vanish. If you don't have a starter cushion yet, this is a fast way to begin building your emergency fund.

No-Spend Challenge vs. a Long-Term Budget

People sometimes ask whether a no-spend challenge replaces a budget. It doesn't - they do different jobs. A budget is the ongoing system that tells every dollar where to go each month. A no-spend challenge is a short, intense reset you drop on top of that system to break a bad pattern or sprint toward a goal. Think of the budget as your training plan and the challenge as a race day. If you want the steady, everyday structure, build it with something like the 50/30/20 budget rule and use no-spend challenges to give it a boost.

A No-Spend Challenge for Every Situation

A no-spend challenge bends to fit almost any money situation. Here's how different people can use it:

- You're trying to save for one specific thing. Run a focused challenge and route every saved dollar toward the goal. Pair it with sinking funds so the money has a clear home, like a holiday fund or a car repair stash.

- You overspend on impulse. Use a strict challenge to break the auto-buy habit, then keep the guardrails that worked. Many people layer it with the cash envelope system to keep variable spending capped after the challenge ends.

- You just got a windfall. Before lifestyle creep eats it, run a short no-spend challenge to stay grounded and put the money to work. Our guide on what to do with a tax refund pairs well with this.

Beginner, Intermediate, and Advanced No-Spend Setups

If you're a beginner, run a 7-day soft challenge with a short off-limits list, like dining out and online shopping. The goal is one clean win you can build on. If you're intermediate, step up to a 14- or 30-day challenge with a tighter rulebook and a dollar target you track daily. If you're advanced, run a recurring monthly challenge, or stack a strict 30-day reset on top of a full budget and funnel the savings straight into investing or debt payoff.

Personalizing Your No-Spend Challenge in 2026

The version that sticks is the one built around your real life. If most of your leaks happen on your phone in 2026, your challenge should start there - mute shopping notifications, log out of one-tap checkout, and unsubscribe from the marketing emails that nudge you. If your spending is social, plan free ways to see friends during the window so you're not white-knuckling every invite. A good budgeting app can make tracking painless; see our roundup of the best budgeting apps to find one that fits.

Frequently Asked Questions

How much money can you actually save with a no-spend challenge?

It depends on your usual discretionary spending, but most people save a few hundred dollars in a 30-day challenge. If you typically spend $10 to $15 a day on extras, a strict month-long no-spend challenge can keep $300 to $450 in your pocket. The key is moving that money to savings right away, before it gets quietly re-spent.

What counts as essential during a no-spend challenge?

Essentials are the things you truly need to live and meet your obligations: rent or mortgage, utilities, insurance, transportation to work, medication, and basic groceries. Everything else - takeout, entertainment, clothing, gadgets, and impulse buys - is non-essential. The exact line is yours to draw, but write it down before you start so you're not negotiating with yourself mid-challenge.

Will a no-spend challenge hurt my credit or finances?

No. A no-spend challenge only pauses optional purchases, so you keep paying rent, bills, and minimum debt payments on time, which protects your credit. If anything, it helps your finances by freeing up cash. Just be sure to keep all required payments flowing - the challenge is about cutting wants, never skipping obligations.

Final Thoughts

A no-spend challenge is the fastest way we know to reset a leaky budget and prove to yourself that those small, forgettable purchases were costing real money. Set your rules, pick a window, protect your essentials, and move every saved dollar somewhere it can grow. Done once, it's a quick win. Done regularly in 2026, it's a habit that quietly builds wealth.

Here's why this approach works for everyday earners:

- Plain-language guidance. No jargon, no shame - just a simple system you can set up in an afternoon.

- Real numbers and examples. We show you what the savings actually look like, from $360 a month to a fully funded goal.

- Proven, time-tested methods. A spending freeze is one of the oldest, most reliable budgeting resets there is.

- Free, practical tools and guides. Everything you need to run your first challenge is right here, at no cost.

Ready to start? Pick your window, write your rules tonight, and put your savings plan in motion with more free guides at Wealth Builder Daily. For unbiased help building the budget your challenge plugs into, the Consumer Financial Protection Bureau offers free tools and worksheets worth bookmarking. Your next financial win can start with a single no-spend day.

The Newsletter

Get the Free Budget Tracker

Join our weekly newsletter. Practical money guides, no fluff. Unsubscribe anytime.