Pay Yourself First: The Automatic Savings System That Builds Wealth in 2026

Pay yourself first means moving money into savings or investments the moment your paycheck lands — before you pay a single bill or spend a dollar on anything else. It flips the usual order of money management on its head, and that one small change is the reason it works when willpower fails.

If you have ever reached the end of the month planning to save "whatever is left over" only to find nothing left, this guide is for you. We will cover what paying yourself first actually means, how much to set aside, where to put the money, and how to automate the whole thing so it runs in the background in 2026 without you thinking about it.

Pay Yourself First at a Glance

The idea is simple: treat your savings like your most important bill, and pay it before everything else. Most people pay rent, utilities, and credit cards first and save with the scraps. Paying yourself first puts your future at the front of the line. Here are the quick answers to the questions people ask first.

| Question | Quick Answer | | --- | --- | | What does "pay yourself first" mean? | Move money to savings or investing the moment you get paid — before bills or spending. | | How much should I pay myself first? | Start with 10–20% of take-home pay; even 5% beats $0 if money is tight. | | Where should the money go? | A high-yield savings account, a Roth IRA, or your 401(k) — set on autopilot. | | Why does it work? | It removes willpower: you never see the money, so you never get the chance to spend it. | | When should I start? | Your very next paycheck — small and automatic beats big and someday. |

A few things to keep in mind before you set it up:

- Automation does the heavy lifting. A scheduled transfer on payday means the decision is made once, not relived every month.

- The percentage matters more than the dollar amount. Saving 15% of a small paycheck builds a stronger habit than saving a random $50 when you happen to remember.

- Your emergency fund comes first. If you do not have one yet, point your first dollars there. Our guide to building an emergency fund walks through the targets step by step.

- It works at any income. Paying yourself first is a habit, not a salary level.

We Have Watched This One Habit Change Everything

At Wealth Builder Daily, we have spent years helping everyday people move from living paycheck to paycheck to quietly building real savings — and the single change that moves the needle most often is this one. People who try to save with leftover money almost never do, because by the end of the month there is rarely anything left. People who automate a transfer on payday almost always succeed, because the money is gone before they can talk themselves out of it. In this guide, we will show you exactly how to build that system, how to choose the right percentage for your situation, and where to send the money so it actually grows instead of sitting still.

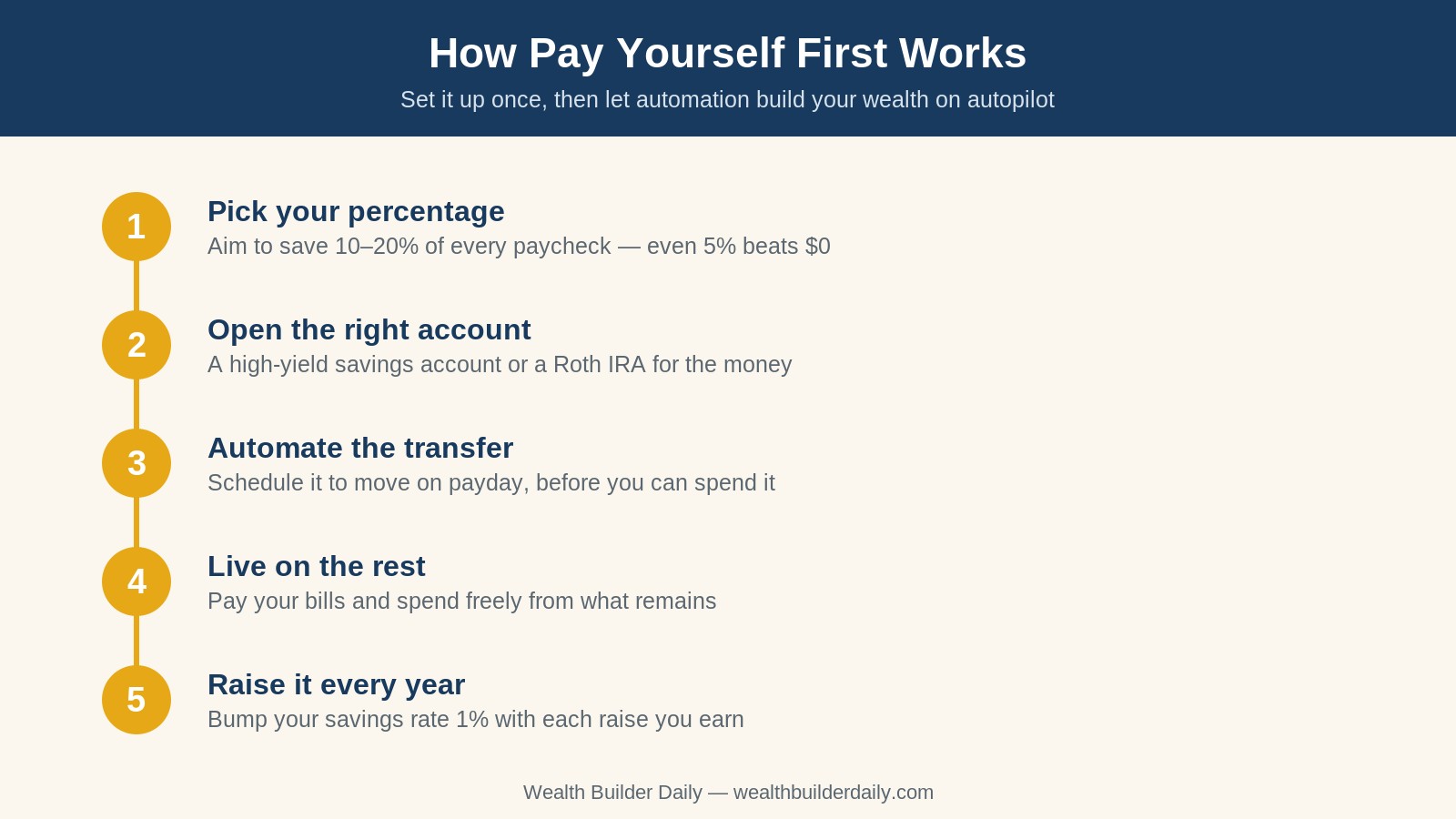

How Pay Yourself First Works

Pay yourself first works by changing the order of operations on payday. Instead of income minus expenses equals savings, you flip it to income minus savings equals what you are free to spend. The mechanism is behavioral, not mathematical — and that is the whole point.

When your savings transfer happens automatically before you ever touch the money, three things change at once. You stop relying on willpower at the end of a long, expensive month. You quietly adjust your spending to the smaller number that is left, the same way you would if you simply earned a little less. And your savings grow on a fixed schedule instead of by accident or good intentions.

Think of it like a Netflix subscription you actually want. You do not agonize over your streaming bill every month — it just comes out, and you live around it. Paying yourself first treats your savings the exact same way: a non-negotiable charge that happens whether you are motivated or not. Here are the key components that make the system run:

- A trigger: your payday, which is the moment the transfer fires.

- A destination: a separate account the money moves into, ideally one you do not check every day.

- An amount: a fixed percentage or dollar figure that comes out every single time, no exceptions.

- Automation: a recurring transfer or direct-deposit split that takes you out of the loop entirely.

The beauty is that once it is built, it keeps working whether you are paying attention or not. You can go three months without thinking about it and still come out ahead — which is exactly what you want from a wealth-building habit.

How to Choose Where Your First Dollars Go

Paying yourself first only pays off if the money lands somewhere useful. Sending it to a checking account you raid every weekend defeats the purpose. Here is how to decide where your first dollars should go, in order of priority.

- Cover a starter emergency fund. Before anything else, get $1,000 set aside for surprises. This keeps a flat tire or a vet bill from turning into credit card debt and undoing your progress.

- Capture any 401(k) match. If your employer matches contributions, that is an instant return you cannot beat anywhere else. Our breakdown of the 401(k) employer match explains why leaving it on the table is the same as turning down a raise.

- Build the full emergency fund. Work toward three to six months of expenses in a high-yield savings account, where it earns real interest while staying completely liquid.

- Fund a Roth IRA. Once your safety net is solid, a Roth IRA lets your savings grow tax-free for decades — one of the best deals in personal finance.

- Invest the rest. With the basics covered, extra dollars can go into low-cost index funds for long-term growth. The federal Investor.gov site is a solid, ad-free place to learn the basics first.

Expert tip: Automating even $200 a month — about $50 a week — adds up to $2,400 a year before any interest. Park that in an account paying around 4% APY in 2026 and you earn roughly $90 in your first year without lifting a finger, and far more as the balance grows and compounds. The number feels small at the start and surprisingly large a few years in. If you want a clear sequence for all of this, our financial order of operations lays out every step in plain language.

To make the choice concrete, here is how the most common destinations compare:

| Destination | Best For | Typical 2026 Return | Access to Money | | --- | --- | --- | --- | | High-yield savings | Emergency fund, short-term goals | ~4% APY | Anytime | | 401(k) with match | Free employer money | Match plus market growth | Retirement age | | Roth IRA | Long-term tax-free growth | Market growth (~7% average) | Contributions anytime | | Brokerage account | Extra investing after the basics | Market growth (~7% average) | Anytime |

Pay Yourself First vs. Paying Off Debt First

This is the most common either/or question, and the honest answer is that you do both at once. Always pay yourself first enough to capture a 401(k) match and a small emergency cushion — that part is non-negotiable. Beyond that, if you carry high-interest debt like credit cards charging 20% or more, throw extra dollars at the debt before investing, because no safe investment beats a guaranteed 20% saved. Once the high-interest debt is gone, redirect those same automated dollars straight into savings and investing without missing a beat.

Pay Yourself First for Every Situation

No two budgets look the same, so the right setup depends on where you are standing right now.

- Steady paycheck: Split your direct deposit so a fixed percentage lands in savings automatically before the rest hits checking. You never see it, so you never miss it.

- Irregular or freelance income: Save a percentage of every payment as it arrives rather than a flat monthly amount. Our irregular income budgeting guide shows how to smooth out the highs and lows so saving still happens in a lean month.

- Tight budget with little margin: Start at 1% and raise it slowly. The habit is what matters; the amount catches up. Pairing this with sinking funds helps you plan for big expenses without raiding what you have saved.

Beginner, Intermediate, and Advanced Setups

A beginner setup is one automatic transfer of 5–10% into a single high-yield savings account on payday. An intermediate setup splits the money — part to the emergency fund, part to a Roth IRA — often 15% in total. An advanced setup automates everything at once: emergency fund topped off, retirement contributions on schedule, and any extra swept into a brokerage account, usually 20% or more of income flowing without a single manual step.

Personalizing Your Plan in 2026

The right number is the one you will actually stick with. In 2026, with high-yield savings still paying around 4% and most banks and budgeting apps offering automatic transfers for free, there has never been an easier time to set this up. Start where you can, automate it today, and raise your rate by one percentage point every time you get a raise. You will barely feel the increase, and your future self will notice the difference. A good budgeting app can track the whole thing for you and show your savings climbing month over month.

Frequently Asked Questions

How much should I pay myself first if I am living paycheck to paycheck?

Start with 1% to 5% of your take-home pay, even if that is just $10 or $20 a paycheck. The goal at first is the habit, not the size of the number. Once the automatic transfer feels normal, raise it slowly — a single percentage point at a time — and bump it up whenever your income grows so saving keeps pace.

Where is the best place to keep money I pay myself first?

For an emergency fund or short-term goals, a high-yield savings account is ideal because it earns around 4% APY in 2026 while keeping your cash available. For long-term, tax-free growth, a Roth IRA is hard to beat. Keep this money in a separate account from your everyday checking so you are not tempted to spend it.

Should I pay myself first before paying off debt?

Save enough to grab any 401(k) match and a small $1,000 cushion first, then focus extra money on high-interest debt. Credit cards charging 20% or more cost you more than savings can earn, so clearing them is its own form of paying yourself. After the costly debt is gone, redirect those automatic payments back into savings.

Final Thoughts

Paying yourself first is the rare money habit that asks for one decision and then rewards you for years. You set the percentage, you automate the transfer, and you let the system quietly build your savings while you get on with your life. The leftover-money approach almost never works; the pay-yourself-first approach almost always does, because it never gives your spending the chance to win.

Here is why this approach works so well:

- Plain-language guidance: No jargon and no shame — just a clear system you can set up this week.

- Real numbers and examples: From $10 a paycheck to a full 20% split, you can see exactly what to do at any income level.

- Proven, time-tested methods: Paying yourself first has built wealth for generations because the behavior, not the market, does the work.

- Free practical tools and guides: Everything you need to start is already free inside your bank or budgeting app.

Your next paycheck is the best place to start. Set up one automatic transfer today, then keep learning with more free guides on the Wealth Builder Daily blog. For unbiased background on saving and account types, the federal Consumer Financial Protection Bureau is a trustworthy place to dig deeper. Pay yourself first, automate it, and let 2026 be the year your savings finally grows on autopilot.

The Newsletter

Get the Free Budget Tracker

Join our weekly newsletter. Practical money guides, no fluff. Unsubscribe anytime.