Cash Envelope System: How to Stop Overspending and Save More in 2026

The cash envelope system is a budgeting method where you divide your spending money into labeled envelopes of physical cash (one per category) and spend only what's inside each one. When an envelope is empty, you're done spending in that category until next month. It's simple, it's old-school, and in 2026 it's still one of the most effective ways for everyday people to stop overspending.

If your money keeps disappearing before the next paycheck and you can't quite explain where it went, this guide is for you. We'll cover exactly how the cash envelope system works, who it helps most, how to choose your categories, and how to make it stick.

Cash Envelope System at a Glance

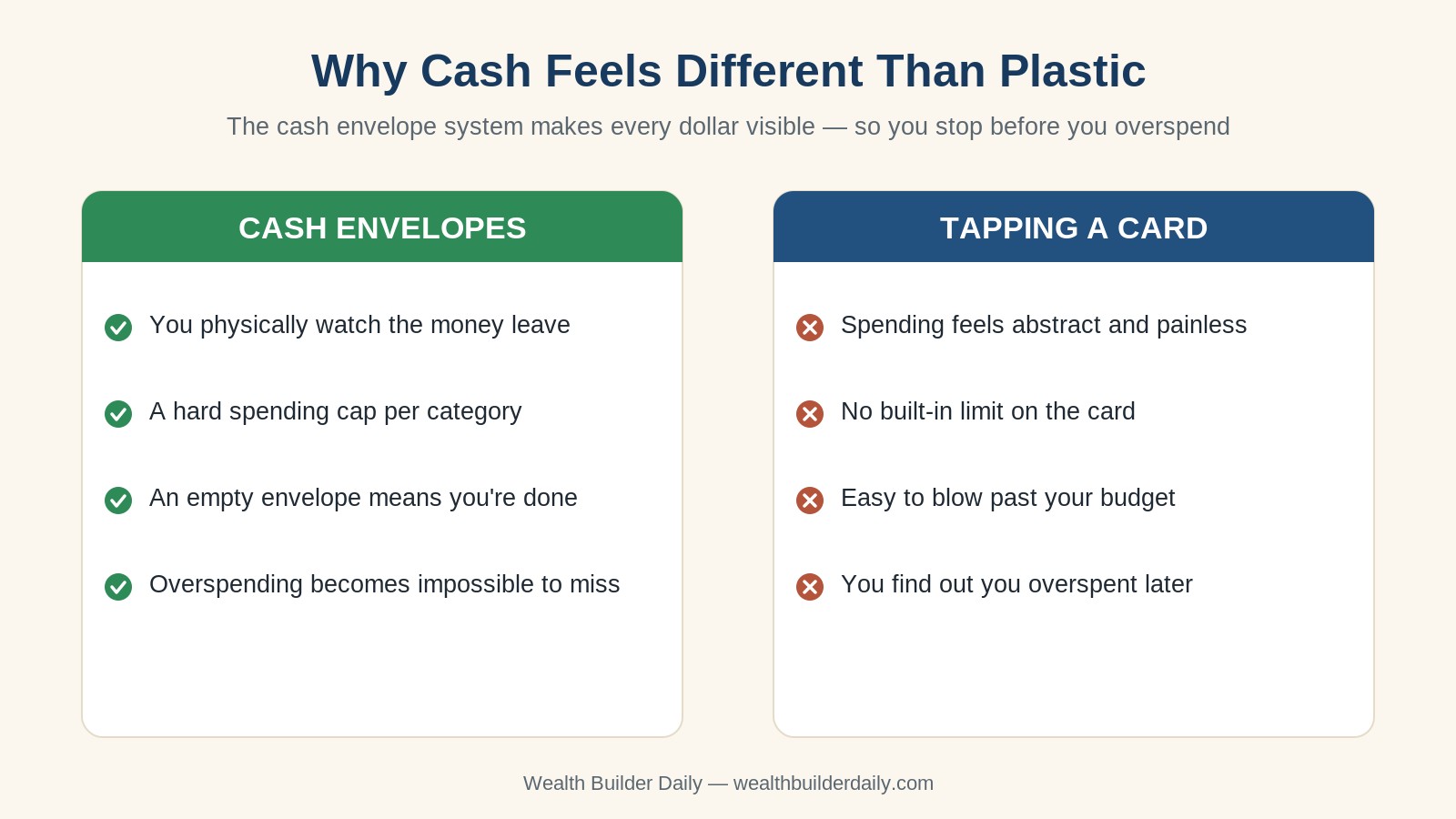

Here's the short version: instead of swiping a card and hoping the math works out, you withdraw cash, split it into envelopes, and let the envelopes enforce your limits for you. The physical act of handing over cash, and watching an envelope get thin, does what a banking app rarely can. It makes overspending impossible to ignore.

| Question | Short Answer | |---|---| | What is it? | A budget where each spending category gets a set amount of cash in its own envelope | | Who is it best for? | Overspenders, card swipers, and anyone who wants a hard limit | | What does it cost? | Nothing - just envelopes and a few minutes a month | | Which categories work? | Variable spending like groceries, dining out, gas, fun money, and personal care | | How long to set up? | About 20 minutes for your first month |

A few quick facts before we dig in:

- It works best for variable spending you tend to overshoot, not fixed bills like rent or insurance.

- You can run it with real cash or with a "digital envelope" app if you prefer to keep your card.

- Most people start with three to five envelopes, not a dozen.

- The system pairs naturally with a broader plan like the 50/30/20 budget rule.

Why the Cash Envelope System Works

The cash envelope system keeps coming up in personal finance circles because it removes the biggest weakness in most budgets: the gap between deciding to spend less and actually feeling it in the moment. In this guide, we'll walk you through how it works, how to choose your envelopes, and how to choose the right version for your life in 2026.

The reason it works is behavioral, not mathematical. Studies on spending consistently find that people spend more when payment feels painless - and few things are more painless than a tap-to-pay card. Cash reintroduces friction. You see the money leave your hand, and you feel the envelope getting lighter. That small jolt of awareness is enough to change decisions before you make them.

How the Cash Envelope System Works

The mechanics are refreshingly simple. You don't need an app, a course, or any financial background to run it. Here are the core pieces of the system:

- Take-home pay - the money that actually lands in your account, after taxes and deductions

- Spending categories - the handful of areas where your money tends to leak

- Envelopes - one labeled envelope per category, holding that category's cash

- The empty-envelope rule - when an envelope runs out, that category is closed for the month

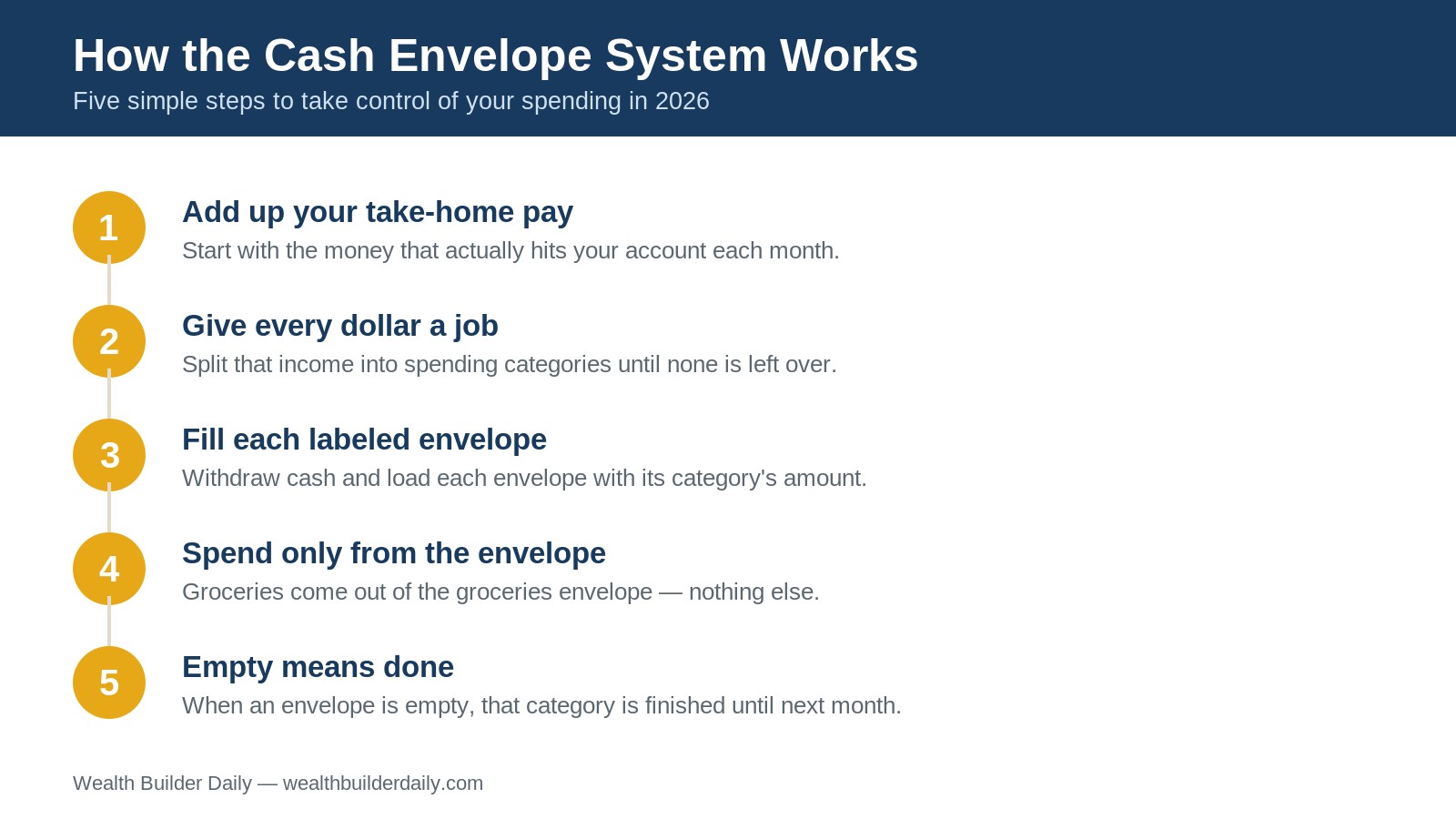

Put together, the process looks like this. You start with your monthly take-home pay, give every dollar a job by assigning it to a category, then withdraw cash and fill each labeled envelope with its amount. From there, you spend only from the matching envelope - groceries come out of the groceries envelope and nowhere else. When an envelope is empty, you stop. That's the whole system.

The empty-envelope rule is the part that does the heavy lifting. In a normal budget, going $60 over on dining out just shows up as a slightly smaller balance you can rationalize away. With envelopes, an empty "dining out" envelope on the 22nd means you're cooking at home for the rest of the month. The limit isn't a number on a screen - it's a fact in your hand.

How to Choose the Right Envelopes for Your Budget

The system only works if your categories match your real spending. Here are the steps to set yours up the right way:

- Start with one month of actual spending. Pull up your last 30 days of transactions and group them. You're looking for the categories where you consistently overshoot - that's where envelopes help most.

- Pick three to five variable categories. Common ones are groceries, dining out, gas or transport, fun money, and personal care. Don't try to envelope everything; fixed bills like rent stay on autopay.

- Assign a realistic amount to each. Base it on what you actually need, not a fantasy number. If you spend $500 on groceries, don't budget $300 and set yourself up to fail.

- Leave fixed bills out of the system. Rent, utilities, insurance, and subscriptions are predictable, so they don't need envelopes. Keep those in your checking account.

- Build in a small buffer. Add a "miscellaneous" envelope of $40 to $60 so one surprise doesn't blow up the whole plan.

- Withdraw the cash and fill the envelopes. Make one trip to the ATM at the start of each month and load every envelope at once.

A quick expert tip: don't over-engineer it. The most common reason people quit the cash envelope system is having too many envelopes. Five categories you'll actually maintain beat fifteen you'll abandon by week two. If you want help separating the categories that deserve an envelope from the ones that don't, our zero-based budgeting guide walks through the full process of giving every dollar a job.

Cash Envelopes vs. Digital Envelopes: Which Is Better?

Traditional cash envelopes use real bills, and that physical friction is exactly why they work. But cash isn't practical for everyone in 2026 - plenty of spending happens online, and carrying cash feels risky to some people. Digital envelope apps recreate the same category limits inside your phone, letting you keep your card while still enforcing a hard cap.

Which should you choose? If overspending is your core problem, start with real cash for at least one month. The discomfort is the point, and it retrains your habits faster than a screen ever will. Once the behavior sticks, you can move to a digital version for convenience. You can compare app options in our roundup of the best budgeting apps for 2026.

The Cash Envelope System for Every Situation

There's no single "right" way to run this system - the best setup depends on how you earn and spend.

- If you're a chronic overspender: Go all-cash for your top two problem categories first. Trying to fix everything at once usually backfires. Master groceries and dining out, then expand.

- If you have an irregular income: Base your envelope amounts on your lowest typical month, not your best one. Our guide to budgeting on an irregular income explains how to build a baseline you can count on.

- If you're saving for a specific goal: Add a dedicated savings envelope and treat it like a bill - fill it first, before the spending envelopes. This is how the envelope system quietly turns into a wealth-building habit.

Beginner, Intermediate, and Advanced Setups

The cash envelope system scales with you. Here's how it tends to grow:

- Beginner: One or two cash envelopes for your worst categories. The goal is simply to stop the bleeding and build the habit of checking before you spend.

- Intermediate: A full set of three to five envelopes covering all your variable spending, refilled on a consistent monthly schedule. At this stage the system is running your discretionary budget.

- Advanced: Spending envelopes plus dedicated savings and sinking-fund envelopes for big future expenses. Combine it with sinking funds and you're not just controlling spending - you're funding your goals on purpose.

Personalizing the System in 2026

One shift worth noting in 2026: more banks now let you create multiple named sub-accounts or "buckets" for free, which act like digital envelopes straight from your existing checking account. You can tailor the system to your life by mixing methods - cash for the categories where you overspend, and automatic transfers into named buckets for savings goals you don't want to touch.

Frequently Asked Questions

How much cash should I put in each envelope?

Base each envelope on your real average spending for that category, not an aspirational target. Look at your last one to three months, take a typical figure, and trim it slightly if you want to push your savings. Starting realistic is what keeps you from quitting in week one.

What do I do when an envelope runs out of money?

You stop spending in that category until next month - that's the rule that makes the system work. If you truly can't (say groceries run out), borrow from your miscellaneous envelope or pull from a lower-priority one like fun money, then adjust next month's amounts. Never reach for a credit card to refill it.

Can I use the cash envelope system with a credit card?

Yes, but carefully. You can keep your card and use a digital envelope app or named sub-accounts to enforce the same category limits, which is ideal for online spending. Just make sure you can pay the balance in full each month - the goal is control, and carrying a balance defeats the purpose.

Final Thoughts

Getting control of your money doesn't require a finance degree, a complicated app, or willpower you don't have. The cash envelope system works precisely because it's simple and physical - it puts a hard, visible limit on the spending that tends to slip away from you, and it gives you the quiet confidence of knowing exactly how much you have left. For a lot of people, the first month with envelopes is the first time their budget actually feels real.

Here's what you can expect from Wealth Builder Daily:

- Plain-language, no-jargon guidance - we explain money the way a friend would, not a textbook.

- Real numbers and real examples - every strategy we share is built for actual everyday budgets.

- Proven, time-tested methods - we focus on what reliably works, not the latest gimmick.

- Free, practical tools and guides - everything you need to build wealth, at no cost.

Ready to take the next step? Explore our full library of budgeting guides and money tools to build a plan that fits your life - and discover how small, consistent habits like this one add up to real wealth over time. For more on the behavioral side of spending, the Consumer Financial Protection Bureau also offers free, unbiased budgeting resources worth bookmarking.

The Newsletter

Get the Free Budget Tracker

Join our weekly newsletter. Practical money guides, no fluff. Unsubscribe anytime.