HSA Investing: How to Build a Tax-Free Retirement Fund in 2026

HSA investing is the quiet way everyday savers turn a basic health account into a tax-free retirement fund — money that goes in before taxes, grows tax-free, and comes out tax-free for medical costs. Most people use a Health Savings Account like a checking account for co-pays. The savers who build real wealth do the opposite: they invest the balance and let it compound for decades.

This guide is for anyone with a high-deductible health plan who wants their HSA to do more than sit in cash. You'll learn exactly how HSA investing works, the 2026 contribution limits, how to pick a provider, and how to match the strategy to your stage of life.

HSA Investing at a Glance

Here's the short answer: an HSA is the only account in the U.S. tax code that is tax-free on the way in, while it grows, and on the way out. That "triple tax advantage" is why it can outperform a 401(k) or Roth IRA for the right person. The table below shows how it stacks up against the accounts you already know.

| Account | Going in | Growth | Qualified withdrawals | Best use | | --- | --- | --- | --- | --- | | HSA | Pre-tax | Tax-free | Tax-free (medical) | Health + retirement, triple tax-free | | Roth IRA | After-tax | Tax-free | Tax-free | Tax-free retirement income | | Traditional 401(k) | Pre-tax | Tax-deferred | Taxed as income | Lowering today's tax bill | | Taxable brokerage | After-tax | Taxed yearly | Capital gains tax | Flexibility, no limits |

A few quick facts to anchor your 2026 plan:

- 2026 limits: you can contribute $4,400 (self-only) or $8,750 (family), plus an extra $1,000 catch-up if you're 55 or older.

- It rolls over forever. Unlike a Flexible Spending Account, an HSA has no "use it or lose it" rule — every dollar stays yours for life.

- Payroll contributions dodge FICA too. Money contributed through your employer's payroll skips the 7.65% Social Security and Medicare tax, a perk no IRA or 401(k) offers.

- After 65, it acts like a 401(k). You can withdraw for anything, penalty-free (non-medical withdrawals are simply taxed as income). Pairing it with your financial order of operations makes the sequence clear.

The Triple Tax Advantage, Explained

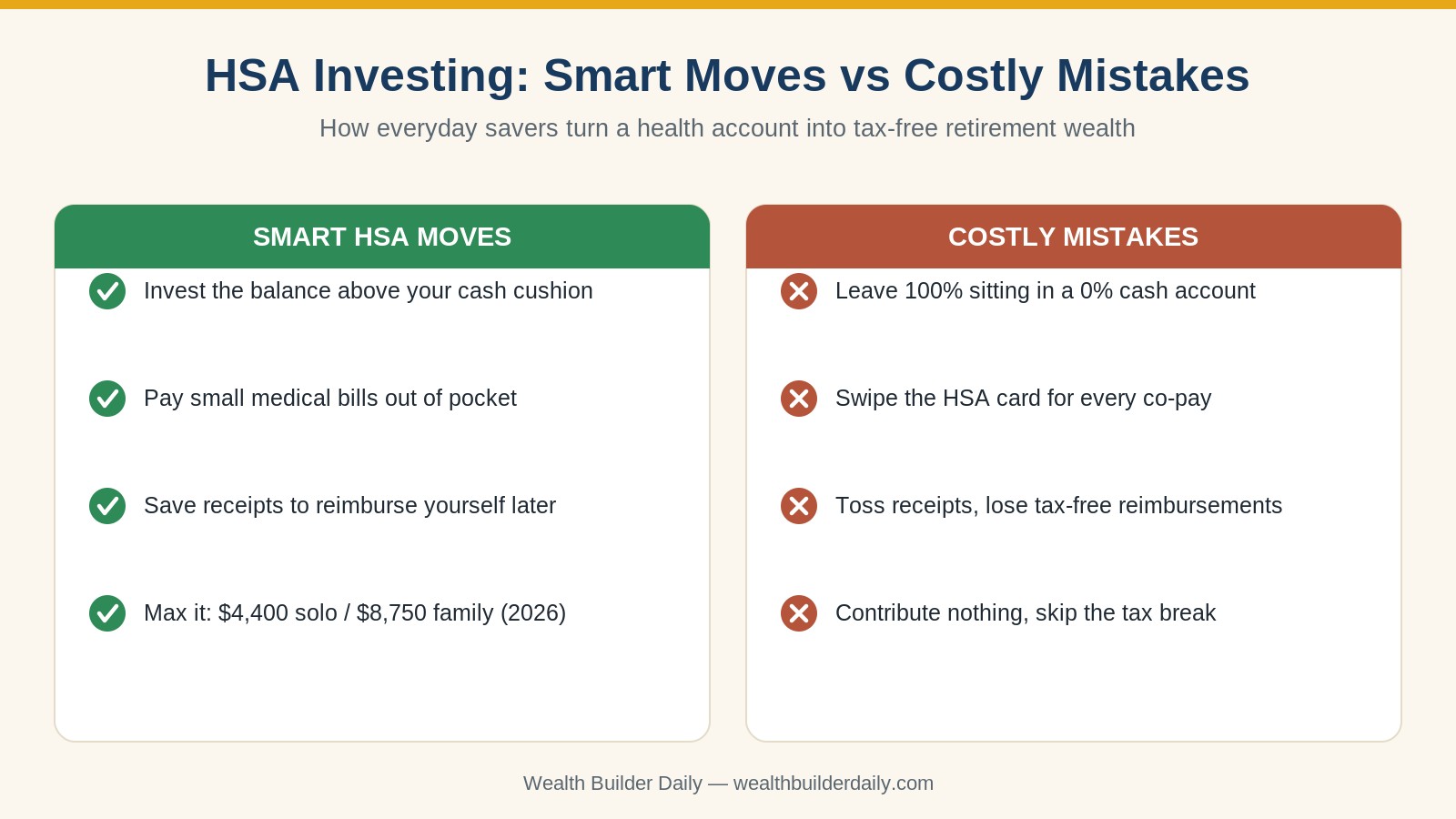

At Wealth Builder Daily, we've spent years helping everyday people turn ordinary accounts into long-term wealth, and the HSA is the one tool almost no one uses to its full potential. In this guide, we'll walk you through how to flip your HSA from a spending card into an investment account — the exact move that separates people who retire with a tax-free medical war chest from people who leave thousands on the table. The graphic below shows the smart moves on one side and the costly mistakes on the other.

How HSA Investing Works

HSA investing works by treating the account as two buckets: a small cash cushion for near-term medical bills, and an invested portfolio for everything above it. Once your balance clears your provider's investing threshold, you move the surplus into funds — usually low-cost index funds or ETFs — and let it grow untouched.

The mechanics break down into a few key parts:

- Eligibility through an HDHP. You can only contribute while covered by an HSA-qualified high-deductible health plan. For 2026, that means a deductible of at least $1,700 (self-only) or $3,400 (family), with out-of-pocket maximums capped at $8,500 and $17,000.

- Pre-tax contributions. Money goes in before income tax, lowering your taxable income for the year — similar to a traditional 401(k), but with the bonus of tax-free withdrawals later.

- Tax-free compounding. Dividends, interest, and capital gains inside the HSA are never taxed, so there's zero tax drag slowing your growth.

- The receipt strategy. Pay small medical bills out of pocket today and save the receipts. Because there's no deadline to reimburse yourself, you can let the money compound for years, then pull out a tax-free lump sum whenever you want.

That last point is the secret weapon. A $300 doctor's visit paid out of pocket in 2026 becomes a $300 tax-free withdrawal you can claim in 2046 — after that money has quietly grown inside index funds for twenty years.

Compare that to an ordinary taxable brokerage account, where every dividend and every sale triggers a tax bill that chips away at your returns year after year. Inside an HSA, none of that drag exists — your full balance keeps compounding. And when you contribute through payroll, you also skip the 7.65% FICA tax, so a single $4,400 contribution can save a typical middle-income worker well over $1,000 in combined income and payroll taxes in one year. Stack those savings across a decade of 2026-and-beyond contributions and the HSA quietly becomes one of the highest-return accounts you own — without the complexity people assume investing requires.

How to Choose the Right HSA Provider

Not all HSAs are built for investing. Many employer-default accounts charge fees or force a large cash balance before you can invest a dime. If you want to actually grow the money, compare providers on these criteria:

- Low or zero investment threshold. Some providers make you keep $1,000–$2,000 in cash before investing the rest. The best ones let you invest from the first dollar, so more of your money compounds.

- No monthly maintenance fee. A $3–$5 monthly fee quietly drains a small balance. Look for accounts that waive it, especially if your employer's plan doesn't.

- A strong investment menu. You want access to broad, low-cost index funds and ETFs with low expense ratios — not a short list of expensive, actively managed funds.

- Simple auto-investing. The ability to automatically sweep anything above your cash target into investments keeps the strategy hands-off.

- Solid app and receipt tracking. Since the receipt method depends on records, a provider that stores your medical receipts digitally is worth a lot.

Here's the expert tip with real numbers: if you invest the full $4,400 self-only limit every year for 25 years and earn a 7% average return, you'd end up with roughly $278,000 — versus about $110,000 if you left it in a 0% cash account. That's around $168,000 in tax-free growth you'd otherwise forfeit. Even maxing a family HSA partway gets you there faster, and you can layer it on top of your 401(k) employer match.

HSA vs. FSA: The Key Difference

People mix these up constantly. A Flexible Spending Account (FSA) is "use it or lose it" — unspent money largely disappears at year-end, and you can't invest it. An HSA rolls over forever, can be invested, and travels with you when you change jobs. If your plan qualifies for an HSA, it is almost always the stronger long-term wealth tool.

HSA Investing for Every Situation

Your ideal approach depends on your health, your cash flow, and how close you are to retirement. The calm, secure outcome below is what consistent HSA investing buys you over time.

- Young and healthy with an HDHP: You rarely hit your deductible, so invest aggressively. Pay the occasional bill out of pocket, save receipts, and let nearly the whole balance compound.

- A family with regular medical costs: Keep a larger cash cushion — maybe one year of your deductible — and invest only the surplus. You still get tax-free growth without risking a cash crunch when bills land.

- Age 55 and nearing retirement: Use the $1,000 catch-up contribution and build a dedicated medical war chest. Healthcare is one of the biggest retirement expenses, and an HSA covers Medicare premiums tax-free. Pair it with a Roth IRA for a fully tax-free income stream.

Beginner, Intermediate, and Advanced Setups

A beginner keeps it simple: contribute enough to invest, then put everything above the cash target into a single target-date or total-market index fund. An intermediate investor automates contributions through payroll to capture the FICA savings and rebalances once a year. An advanced investor maxes the limit, pays all medical bills out of pocket, tracks every receipt for future tax-free reimbursement, and treats the HSA as a stealth retirement account.

Personalizing Your Approach in 2026

The right mix in 2026 comes down to one question: how much medical spending do you actually expect this year? Cover that with cash, then invest the rest. If you're new to choosing funds, a robo-advisor inside your HSA can pick and rebalance a low-cost portfolio for you, so the strategy runs on autopilot.

Frequently Asked Questions

Can I invest my HSA money like a 401(k)?

Yes. Most HSA providers let you invest your balance in mutual funds, index funds, or ETFs once you clear a minimum cash threshold — and some allow investing from the first dollar. The invested portion grows tax-free, just like a 401(k) or IRA, with no taxes on dividends or capital gains along the way.

What happens to my HSA if I never have big medical bills?

Nothing is lost. HSA funds roll over every year and stay yours for life. After age 65, you can withdraw the money for any purpose without penalty — non-medical withdrawals are simply taxed as ordinary income, exactly like a traditional 401(k). Used for healthcare, those withdrawals remain completely tax-free.

Do I have to use an HDHP to keep my HSA?

You only need a qualifying high-deductible health plan to contribute to an HSA, not to keep one. If you switch to a non-HDHP later, you stop adding money but keep the account, keep investing the balance, and keep spending it tax-free on qualified medical costs for the rest of your life.

Final Thoughts

HSA investing is the rare wealth move that costs you nothing extra and quietly compounds for decades — turning a routine health account into a tax-free retirement fund you'll be glad you started in 2026. The difference between spending your HSA and investing it can be six figures by the time you retire.

Here's why everyday savers trust this approach:

- Plain-language guidance. No jargon — just clear steps you can act on this week.

- Real numbers and examples. Concrete 2026 limits and realistic growth math, not vague promises.

- Proven, time-tested methods. The triple tax advantage and index-fund investing are strategies that have worked for decades.

- Free, practical tools and guides. Everything you need to start is on our blog, at no cost.

Your next step is simple: check whether your HSA lets you invest, set a cash target you're comfortable with, and put the rest to work. The earlier you start, the more 2026 becomes the year your health account started building real wealth. Explore more beginner-friendly strategies on the Wealth Builder Daily blog, and review the official rules anytime at Investor.gov.

The Newsletter

Get the Free Budget Tracker

Join our weekly newsletter. Practical money guides, no fluff. Unsubscribe anytime.