How to Invest in Bonds: A Beginner's Guide to Steady Income in 2026

Learning how to invest in bonds is one of the simplest ways to add steady, predictable income to your money — you lend cash to a government or company, and they pay you interest until you get your original money back. If stocks are the growth engine of your portfolio, bonds are the shock absorbers that keep the ride smooth.

This guide is for everyday investors who already have a little money working in stocks or a savings account and want to understand where bonds fit. You'll learn what bonds are, how they actually pay you, the main types to know, and the easiest way to buy your first one in 2026 — no finance degree required.

How to Invest in Bonds at a Glance

Here's the short version: most beginners should invest in bonds through a low-cost bond fund or ETF inside a regular brokerage account, rather than buying individual bonds one at a time. A fund spreads your money across hundreds of bonds automatically, so you get steady interest without the guesswork.

| Bond Type | Best For | Typical Risk | Where to Start | | --- | --- | --- | --- | | U.S. Treasurys | Maximum safety | Very low | TreasuryDirect or a broker | | Municipal bonds | Tax-free income | Low–medium | Brokerage or muni bond fund | | Corporate bonds | Higher yields | Medium | Corporate bond ETF | | Bond funds & ETFs | Hands-off beginners | Low–medium | Any brokerage account |

A few quick facts to anchor you:

- Bonds pay you interest — usually twice a year — called the "coupon."

- You can start small. A single share of a bond ETF often costs $50 to $110, and Treasurys can be bought for as little as $100.

- Bonds and stocks work together. When stocks drop, high-quality bonds often hold steady, which is why they belong in a balanced asset allocation by age.

- Safer than stocks, but not risk-free. Bond prices still move, especially when interest rates change.

We've Helped Everyday Investors Build Balanced Portfolios

At Wealth Builder Daily, we've spent years helping everyday people move past the fear of investing and build portfolios they actually understand. Bonds are one of the most misunderstood pieces of that puzzle — people either ignore them completely or pour in too much, too soon. In this guide, we'll walk you through the smart, plain-language way to use bonds so they do their real job: protecting your money and paying you along the way.

How Investing in Bonds Works

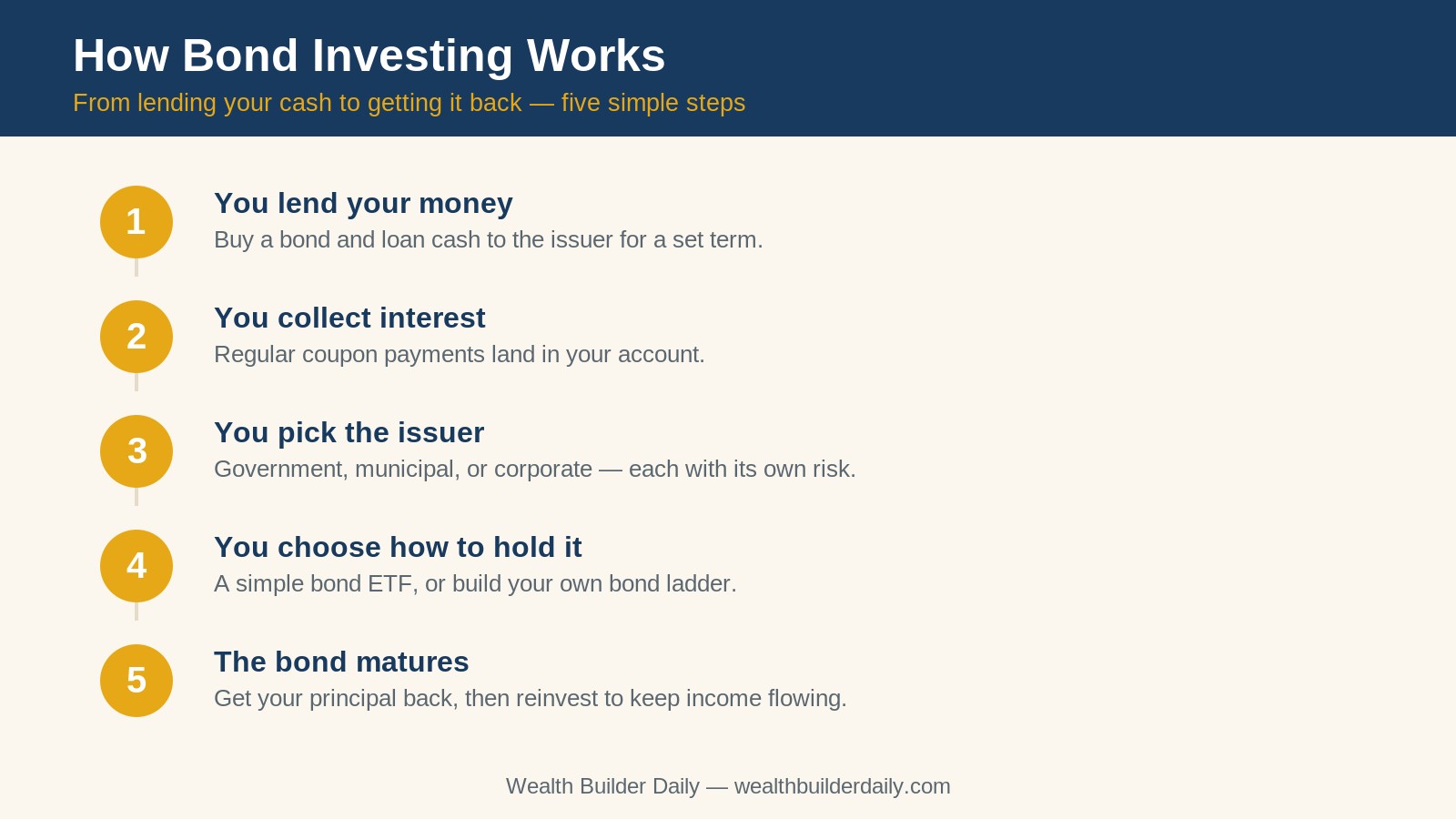

When you invest in bonds, you become the lender instead of the borrower. A government or corporation needs to raise money, so it issues a bond — basically an IOU. You hand over your cash, and in return you get a written promise: regular interest payments plus your original amount (the "principal") back on a set date called the maturity date.

Say you buy a bond worth $1,000 that pays 5% a year over 10 years. Each year you collect $50 in interest, and at the end of year 10 you get your $1,000 back. Over that decade, that single bond paid you $500 in income on top of returning your principal. Multiply that across a fund holding hundreds of bonds, and you have a quiet, steady income stream that keeps arriving whether the stock market is up or down. That reliability is the whole point of owning bonds in the first place.

The key moving parts to understand:

- Coupon rate — the interest the bond pays each year, as a percentage of its face value.

- Maturity — how long until you get your principal back (anywhere from a few months to 30 years).

- Yield — your actual return based on the price you paid, which can differ from the coupon.

- Credit quality — how likely the issuer is to pay you back, rated from AAA (safest) down to junk.

- Interest-rate risk — when rates rise, existing bond prices fall; when rates drop, they rise.

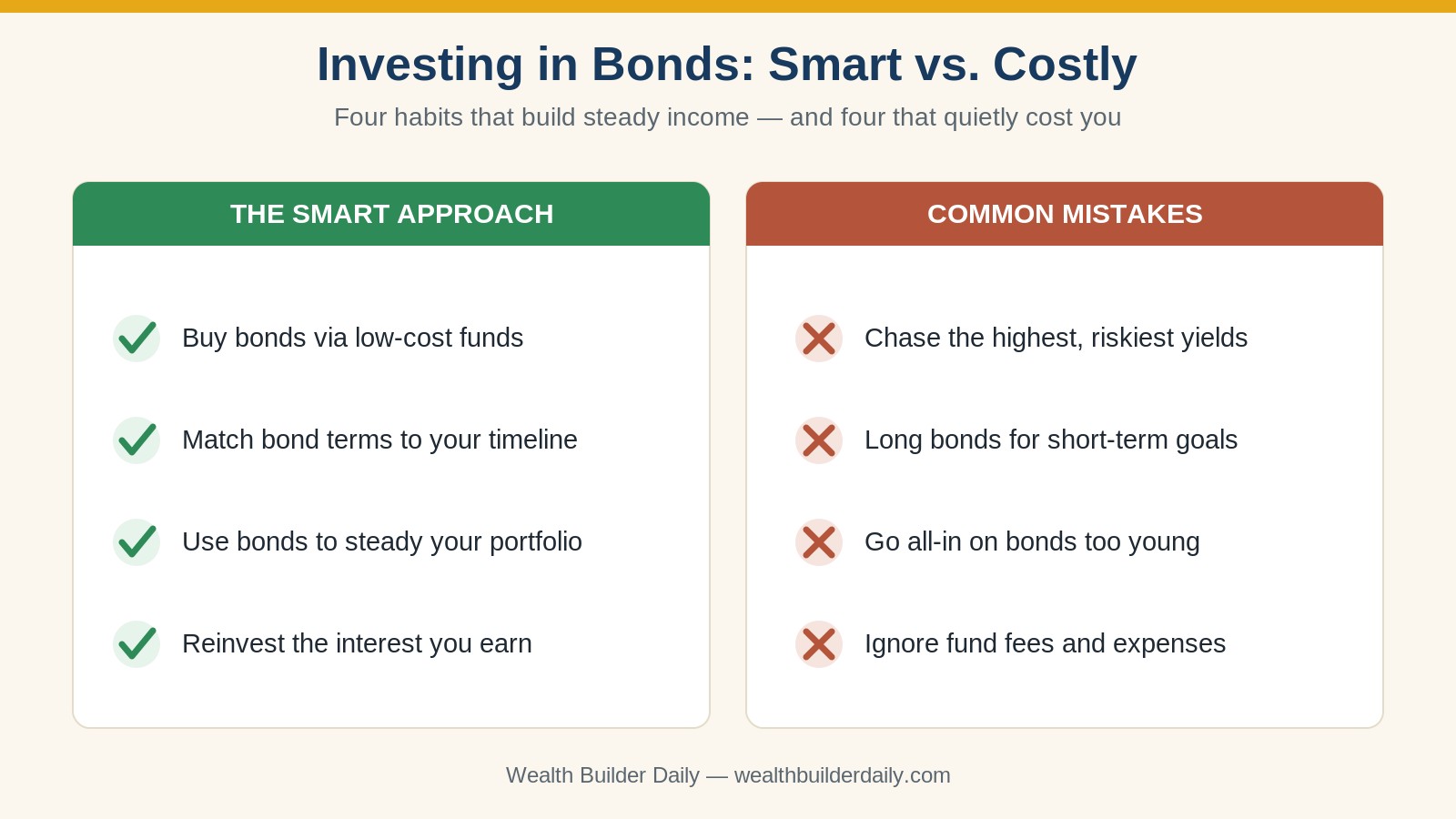

How to Choose the Right Bonds

Not all bonds serve the same purpose. Here's how to narrow it down without overthinking it.

-

Start with your timeline. Money you'll need in one to three years belongs in short-term bonds or a high-yield savings account, not long bonds. Money you won't touch for a decade can handle longer maturities that pay more.

-

Decide safety versus yield. U.S. Treasurys are backed by the federal government and are about as safe as investing gets. Corporate bonds pay more but carry more risk. There's no free lunch — higher yield always means higher risk.

-

Check the credit rating. Stick with investment-grade bonds (rated BBB/Baa or higher) unless you truly understand what you're buying. Chasing a flashy 9% yield often means buying shaky "junk" bonds.

-

Mind the fees. With bond funds, the expense ratio matters. A fund charging 0.05% keeps far more money in your pocket than one charging 0.75% over the years.

-

Match the account to the bond. Taxable corporate and Treasury bonds often work best inside a tax-advantaged account like an IRA, while tax-free municipal bonds shine in a regular brokerage account.

-

Keep it simple to start. A single, broad "total bond market" ETF gives you instant diversification across government and corporate bonds in one purchase.

Here's an expert tip with real numbers: a total bond market ETF in 2026 typically holds more than 10,000 individual bonds and charges around $3 to $5 per year for every $10,000 you invest. Buying that same diversification one bond at a time would take tens of thousands of dollars and hours of research. That's why funds win for almost every beginner. If you don't have a brokerage yet, start by opening your first brokerage account.

Individual Bonds vs. Bond Funds

If you buy an individual bond and hold it to maturity, you know exactly what you'll get back — that predictability is nice for a specific future expense. But it takes real money to diversify, and selling early can mean a loss. A bond fund gives you instant diversification and easy buying and selling for a low fee, though its price floats daily and there's no fixed "payback" date. For most beginners in 2026, a low-cost bond fund is the simpler, safer starting point.

Bond Investing for Every Situation

Your bond strategy should match where you are in life, not a one-size-fits-all rule. The porch you're building toward looks different for everyone.

- The cautious beginner who hates seeing their balance swing should hold a modest slice of bonds — maybe 10% to 20% — as a cushion while the rest grows in index funds and ETFs. That small slice can make a volatile market far easier to sit through without panic-selling.

- The near-retiree in their late 50s or 60s leans more heavily into bonds to protect the nest egg they've spent decades building, shifting the balance from growth toward stability.

- The saver with a known future expense — a house down payment in three years, say — can use short-term Treasurys to earn interest without risking the principal they'll soon need.

Beginner, Intermediate, and Advanced Setups

A beginner can hold everything in one total bond market ETF and be done. An intermediate investor might split holdings between a Treasury fund and a corporate bond fund to fine-tune risk and yield. An advanced investor could build a "bond ladder" — buying bonds that mature in staggered years — so cash comes due at regular intervals for reinvesting or spending.

Personalizing Your Approach in 2026

With interest rates in 2026 sitting well above where they were a few years ago, bonds are paying more than they have in over a decade — which makes this a genuinely better moment to hold them than the near-zero-rate era. Still, don't chase yield blindly. Pick a bond allocation that matches your age, your goals, and how much volatility you can stomach, then automate your contributions and leave it alone. Pairing bonds with a solid emergency fund gives you a durable financial base, so a surprise expense never forces you to sell investments at the worst possible moment. Revisit your mix once a year and nudge it back to your target as your life changes.

Frequently Asked Questions

How much money do I need to start investing in bonds?

Less than you'd think. A single share of a bond ETF often costs between $50 and $110, and U.S. Treasurys can be purchased directly from the government for as little as $100 through TreasuryDirect. You don't need thousands of dollars — you can start with whatever you'd comfortably set aside from one paycheck and add to it over time.

Are bonds safer than stocks?

Generally, yes — especially high-quality government bonds. Bonds tend to hold their value better than stocks during market drops, which is exactly why they belong in a balanced portfolio. But "safer" isn't "risk-free." Bond prices still fall when interest rates rise, and lower-rated corporate bonds carry real risk that the issuer could miss payments.

Should I buy individual bonds or a bond fund?

For most beginners, a low-cost bond fund or ETF is the better choice. One purchase spreads your money across thousands of bonds, keeps fees low, and lets you buy or sell easily. Individual bonds make more sense when you want a guaranteed payout on a specific future date and have enough money to diversify properly on your own.

Final Thoughts

Learning how to invest in bonds isn't about chasing the biggest returns — it's about building a portfolio that can weather storms and keep paying you along the way. Start simple, hold quality, match your bonds to your timeline, and let the steady income do its quiet work while your stocks handle the growth.

Here's why thousands of everyday investors trust Wealth Builder Daily to guide their money:

- Plain-language guidance — we explain bonds, yields, and funds in words that actually make sense, with no confusing jargon.

- Real numbers and examples — every strategy comes with concrete dollar figures so you can picture exactly how it works for you.

- Proven, time-tested methods — we focus on the boring, reliable approaches that have built wealth for decades, not hype or fads.

- Free, practical tools and guides — from beginner explainers to full portfolio walk-throughs, our library is here whenever you're ready to take the next step.

Your next move is simple: pick one small bond fund, make your first contribution, and keep learning. Explore more beginner-friendly investing guides on the Wealth Builder Daily blog, and check out the free, unbiased bond education from the SEC at Investor.gov to keep building your confidence in 2026 and beyond.

The Newsletter

Get the Free Budget Tracker

Join our weekly newsletter. Practical money guides, no fluff. Unsubscribe anytime.