Target-Date Funds for Beginners: The One-Fund Way to Invest for Retirement in 2026

Target-date funds are all-in-one retirement funds that automatically shift from growth toward safety as you get older, so you can invest with a single choice and let it run for decades. If picking individual stocks or building your own mix of funds feels overwhelming, a target-date fund hands that job to a professional formula instead.

This guide is for beginners who want to start investing for retirement without becoming a full-time money manager. You will learn what target-date funds are, how they quietly rebalance themselves, how to choose the right one, and the small mistakes that can cost you real money over a working lifetime.

Target-Date Funds at a Glance

A target-date fund is a single mutual fund or ETF built around the year you plan to retire. You buy one fund, and it holds a diversified mix of stocks and bonds that gradually grows more conservative as that date approaches. Here are the most common questions, answered fast.

| Question | Short Answer | | --- | --- | | What is a target-date fund? | One fund holding a full stock-and-bond mix tied to your retirement year. | | How do I pick one? | Choose the year closest to when you turn about 65. | | What does it cost? | Index-based versions often run 0.08%-0.20% per year; some active ones top 0.50%. | | Who is it best for? | Hands-off investors who want one decision, not a dozen. | | Where do I hold it? | Inside a 401(k), Roth IRA, or regular brokerage account. |

A few quick facts worth remembering in 2026:

- One fund, full diversification. A single target-date fund can hold thousands of stocks and bonds across the globe, similar to the all-in-one approach behind a simple index fund portfolio.

- It rebalances for you. You never have to manually move money from stocks to bonds; the fund does it on a set schedule called a glide path.

- The year is a guide, not a rule. A 2060 fund is built for someone retiring around 2060, but you can pick an earlier or later date to match your own risk comfort.

- Fees still matter. Two funds with the same target year can charge very different amounts, and that gap compounds for decades.

Why Trust This Guide

At Wealth Builder Daily, we have spent years helping everyday people turn confusing financial products into simple, repeatable habits. We have watched new investors freeze at the brokerage screen, unsure which of a hundred funds to buy, and we have seen how much calmer the process becomes when one solid default does most of the work. In this guide, we will walk you through exactly how target-date funds operate, what to check before you buy, and how to avoid the handful of errors that quietly drag down returns. No jargon, no hype, just the plain mechanics and the numbers that matter.

How Target-Date Funds Work

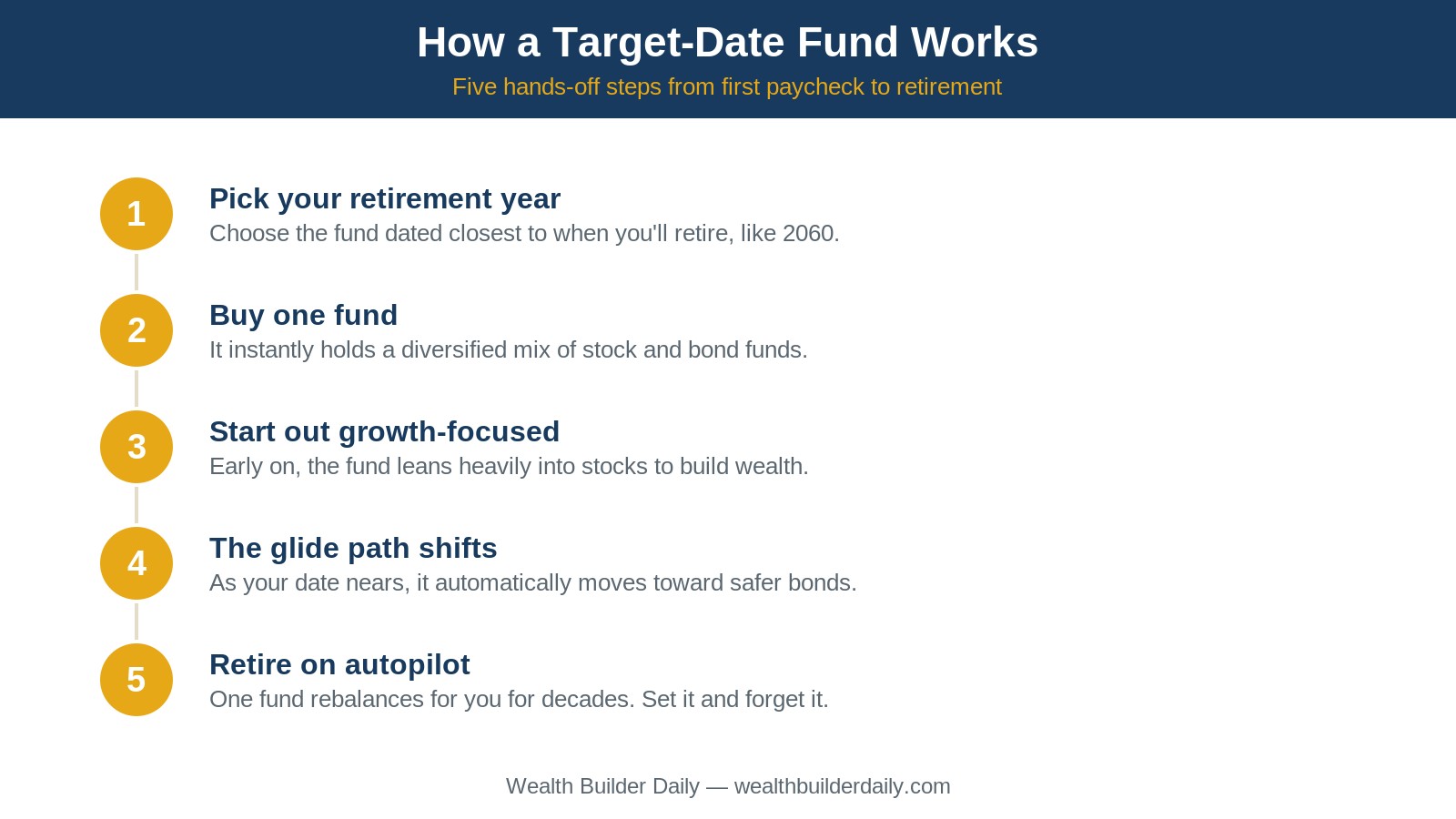

The magic of target-date funds is something called a glide path. When your retirement date is far away, the fund holds mostly stocks, because stocks grow faster over long stretches and you have time to ride out the dips. As your target year gets closer, the fund slowly sells stocks and buys more bonds, which are steadier and protect the money you will soon need. You do nothing. The fund manager follows the glide path automatically, year after year.

Think of it like a flight. Early on, the plane climbs hard for altitude, which is the growth phase heavy in stocks. As you near the destination, the pilot eases the descent so the landing is smooth, which is the shift toward bonds and cash near retirement.

Here are the key components working under the hood:

- A diversified core. Most target-date funds are built from a handful of broad index funds covering U.S. stocks, international stocks, and bonds.

- An age-based glide path. A published schedule decides what percentage sits in stocks versus bonds at every age.

- Automatic rebalancing. When markets move and your mix drifts, the fund resets it back to plan without you lifting a finger.

- A single expense ratio. One yearly fee covers the whole package, expressed as a percentage of what you have invested.

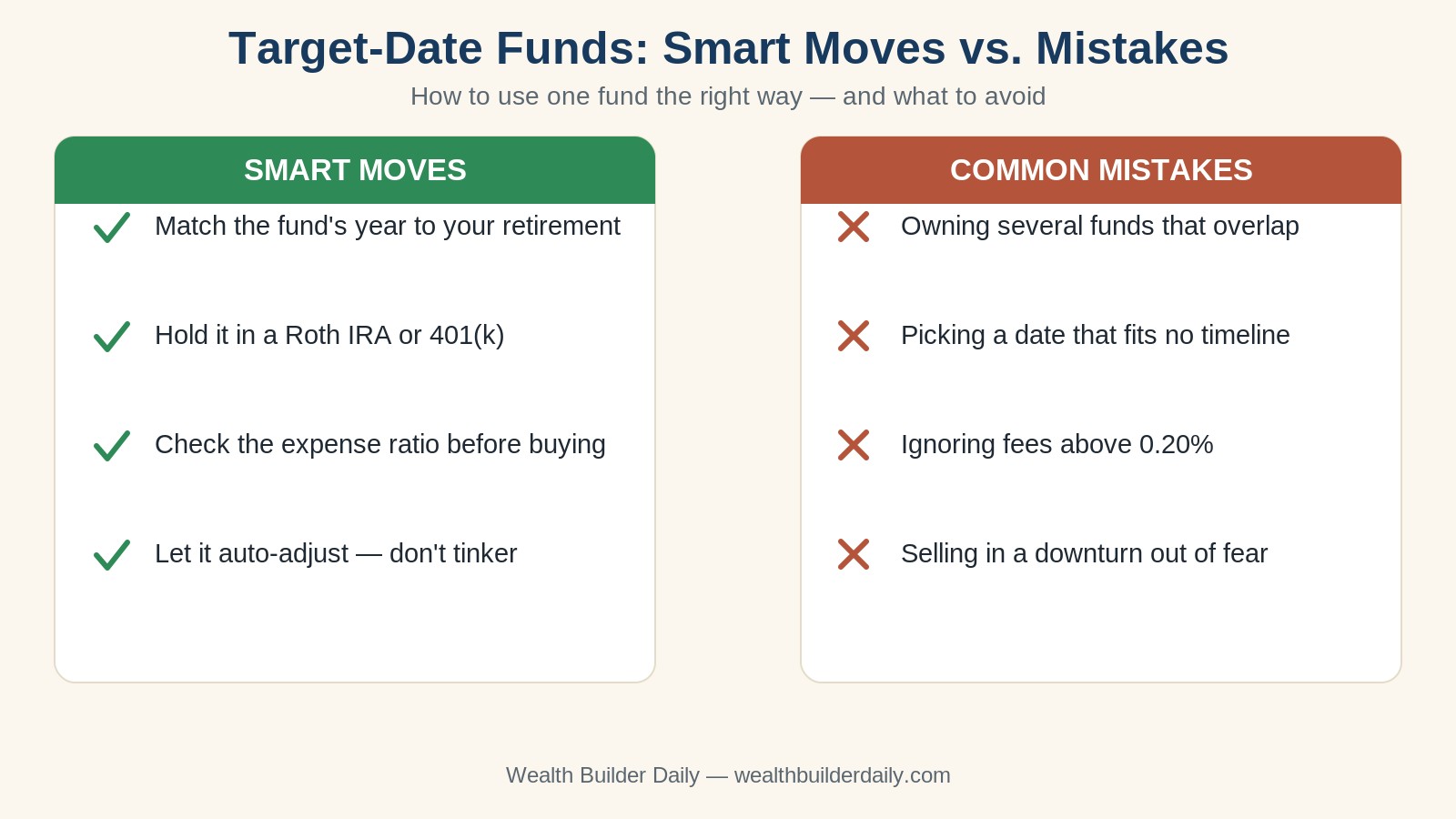

How to Choose the Right Target-Date Fund

Picking a target-date fund is simpler than picking individual investments, but a few choices still make a real difference. Walk through these criteria in order.

- Start with your retirement year. Estimate the year you will turn roughly 65, then round to the nearest fund date. If you are 30 in 2026 and plan to retire around 2061, a 2060 fund is a clean fit.

- Check the expense ratio. This is the yearly fee. Index-based target-date funds in 2026 commonly charge between 0.08% and 0.20%. Anything above 0.50% deserves a hard look, because high fees compound against you over time.

- Look at the glide path style. Some funds reach their most conservative mix "to" retirement; others keep adjusting "through" retirement for years after. Neither is wrong, but it changes how much stock you hold at 65.

- Confirm it is broadly diversified. A good target-date fund spreads money across U.S. and international stocks plus bonds. Read the holdings page to be sure it is not concentrated in one narrow area.

- Match it to the account. You can hold a target-date fund in a Roth IRA, a workplace plan, or a taxable account. In a 401(k), it is often the default option already.

- Keep it as your only retirement fund. Target-date funds are designed to be the whole portfolio. Stacking several on top of each other just creates overlap and confusion.

A quick number to anchor on: a 0.15% expense ratio means you pay about $15 a year for every $10,000 invested. A 0.60% fund charges $60 for the same $10,000. On a $200,000 balance held for 25 years, that fee gap alone can quietly cost you tens of thousands of dollars in lost growth. Before you click buy, compare the fee against a plain index fund so you know what you are paying for the autopilot.

Target-Date Fund vs. Building Your Own Portfolio

Building your own mix of index funds can cost a hair less and gives you full control, but it puts the rebalancing and glide-path decisions on your shoulders forever. A target-date fund trades a tiny bit of extra fee for a system that never forgets to rebalance, never panics in a downturn, and never needs you to log in. For most beginners, that trade is well worth it. If you enjoy the hands-on work and will actually keep up with it, a do-it-yourself portfolio can be a fine alternative.

Target-Date Funds for Every Situation

There is no single "best" target-date fund for everyone, but there is a sensible default for almost every kind of investor. The goal is to match the fund to where you are in life and how much risk lets you sleep at night.

- The brand-new investor. If you just opened your first account, a target-date fund is often the smartest single purchase you can make. It instantly diversifies you and removes the paralysis of choosing among hundreds of options. Pair it with the 401(k) employer match if your job offers one.

- The job-hopper rolling over old accounts. If you have a 401(k) from a former employer, rolling it into an IRA and parking it in one target-date fund keeps your retirement money simple and consolidated instead of scattered.

- The cautious saver near retirement. If your date is close and market swings make you nervous, a target-date fund already leans toward bonds for you, smoothing the ride without forcing you to time anything.

Beginner, Intermediate, and Advanced Setups

A beginner can hold one target-date fund and call the retirement portfolio done. An intermediate investor might keep a target-date fund as the core but add a small slice of something extra, like a broad international fund, once they understand it. An advanced investor who wants precise control over asset allocation by age may eventually build a custom portfolio of separate index funds, but even many advanced savers stick with target-date funds for the discipline they enforce.

Personalizing Your Approach in 2026

The named year on a fund assumes an average risk appetite, so feel free to adjust. If you want more growth and can stomach bigger swings, choose a fund dated a few years later than your actual retirement, which keeps more in stocks. If you want a calmer ride, choose an earlier-dated fund with more bonds. In 2026, with plenty of low-cost index-based options available, you can fine-tune your risk simply by shifting the target year up or down.

Frequently Asked Questions

Are target-date funds a good investment for beginners?

For most beginners, yes. A target-date fund delivers instant diversification, automatic rebalancing, and a built-in glide path in a single purchase. It removes the two biggest beginner traps: choosing wrong and doing nothing. As long as you check the expense ratio and pick a sensible year, it is one of the simplest sound choices in investing.

What happens to my target-date fund when I retire?

The fund does not cash out on your retirement date. It simply reaches its most conservative mix and continues holding a blend of bonds and some stocks to keep growing modestly. You then withdraw money gradually as needed. Many funds keep adjusting for years past the target year, which is the "through retirement" glide path style.

Can I lose money in a target-date fund?

Yes. Target-date funds hold stocks and bonds, and both can fall in value, so your balance can drop in a bad year. They are diversified, which softens the blows, but they are not guaranteed or risk-free. Over long periods the mix is designed to grow, which is why staying invested through downturns matters so much.

Final Thoughts

Target-date funds turn a complicated job into a single, sensible decision: pick the year you plan to retire, buy the fund, and let its glide path do the rest. For beginners who want to invest for retirement without managing it daily, that simplicity is the whole point, and it has powered millions of quiet, steady portfolios into 2026.

Here is why this approach works so well:

- Plain-language guidance. No insider jargon, just clear steps you can act on today.

- Real numbers and examples. We show you exactly how fees and glide paths play out in dollars, not vague promises.

- Proven, time-tested methods. Target-date funds and broad diversification are strategies that have helped ordinary people build wealth for decades.

- Free, practical tools and guides. Everything here is built to help you start now, with no upsell.

Your next step is small but powerful: open your retirement account, find the target-date fund nearest your year, and check its expense ratio before you invest a dollar. For more beginner-friendly walkthroughs on building lasting wealth, explore the full library at Wealth Builder Daily, and lean on a trusted public resource like the SEC's Investor.gov to double-check any fund before you buy. The earlier you let compounding and a steady glide path work together, the more your future self will thank you.

The Newsletter

Get the Free Budget Tracker

Join our weekly newsletter. Practical money guides, no fluff. Unsubscribe anytime.