Dividend Investing for Beginners: How to Build Passive Income From Stocks in 2026

Dividend investing for beginners is simply the practice of buying shares in companies that pay you a slice of their profits, then letting those payments grow your wealth over time. You buy a stock or fund, the company sends you cash every few months, and you decide whether to spend it or reinvest it. That's the whole idea in one sentence.

This guide is for everyday people who want their money to start working as hard as they do. You don't need a finance degree, a huge balance, or hours of free time. You need a clear plan, a little patience, and the willingness to let small payments compound into something meaningful. Below, we'll walk you through how dividends work, how to choose your first investments, and how to avoid the mistakes that trip up most new investors in 2026.

Dividend Investing at a Glance

A dividend is a cash payment a company shares with the people who own its stock. If you own 100 shares of a company that pays $0.50 per share each quarter, you collect $50 four times a year — $200 total — just for holding the stock. Reinvest those payments and your next check is a little bigger, then bigger again. That quiet snowball is the heart of dividend investing for beginners.

Here is how the most common starting points compare:

| Dividend Option | Best For | Typical Yield (2026) | Key Feature | |---|---|---|---| | Dividend ETFs / index funds | Hands-off beginners | 1.5%–3.5% | Instant diversification, very low fees | | Dividend Aristocrats | Steady-growth seekers | 2%–4% | 25+ years of rising payouts | | High-yield stocks | Income-now investors | 4%–7% | Bigger checks, higher risk | | REITs | Real estate income | 3%–6% | Real estate income without owning property |

A few quick facts to anchor you:

- Yield is the annual payout divided by the share price. A $100 stock paying $3 a year yields 3%.

- Most U.S. companies pay quarterly, so you'll often see four payments a year per holding.

- Reinvesting is where the magic lives. The same engine behind compound interest powers dividend growth.

- You can start with one fund. A single diversified dividend ETF can hold hundreds of companies at once.

At Wealth Builder Daily, We Keep Investing Simple

At Wealth Builder Daily, we've spent years helping everyday people turn confusing financial topics into plain, doable steps. We've watched readers go from "I don't even know what a dividend is" to collecting their first payout and reinvesting it without a second thought. In this guide, we'll give you the same framework we'd share with a friend over coffee: what to buy, what to skip, and how to let time do the heavy lifting. No hype, no jargon, just the moves that actually build wealth.

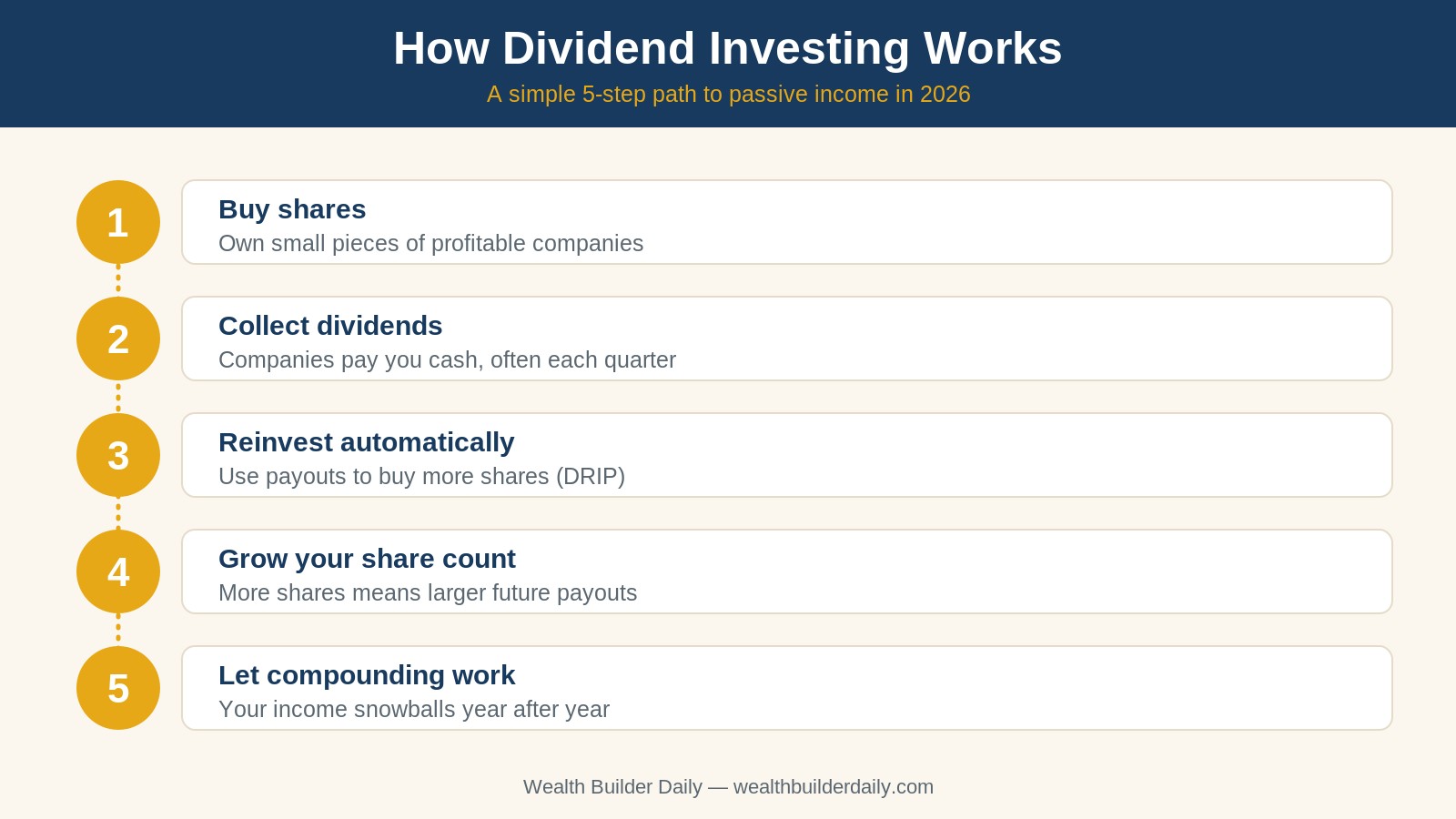

How Dividend Investing Works

When you buy a share of stock, you own a small piece of a real business. Profitable companies often return some of their earnings to owners in the form of dividends. You didn't do anything extra to earn that cash — you simply owned the shares on the right date. That's what makes dividends feel like passive income: the work was done by the business, and you collect the reward.

The real power shows up when you reinvest. Instead of taking the cash, you use it to buy more shares automatically through a dividend reinvestment plan, or DRIP. Those new shares pay their own dividends next quarter, which buy even more shares. Over years, the number of shares you own keeps climbing without you adding a single dollar of your own money.

Here are the key pieces working together:

- Shares: your ownership stake in the company or fund.

- Yield: how much income those shares produce each year as a percentage.

- Payout schedule: usually quarterly, sometimes monthly for certain funds.

- DRIP: the setting that turns every payment back into more shares.

- Time: the ingredient that turns a modest start into a serious income stream.

Picture two investors who each put in $10,000. One pockets every dividend and spends it; the other reinvests automatically. After 20 years at a steady 3% growing yield, the reinvesting investor can end up with thousands of extra dollars and a far larger income stream — without ever adding new money. The takeaway is simple: dividends reward patience. The investor who reinvests for ten years quietly out-earns the one who chases quick wins, because every reinvested payment stacks on the last. In 2026, with automatic reinvestment available on nearly every platform, this used to be hard and is now a single setting you flip once.

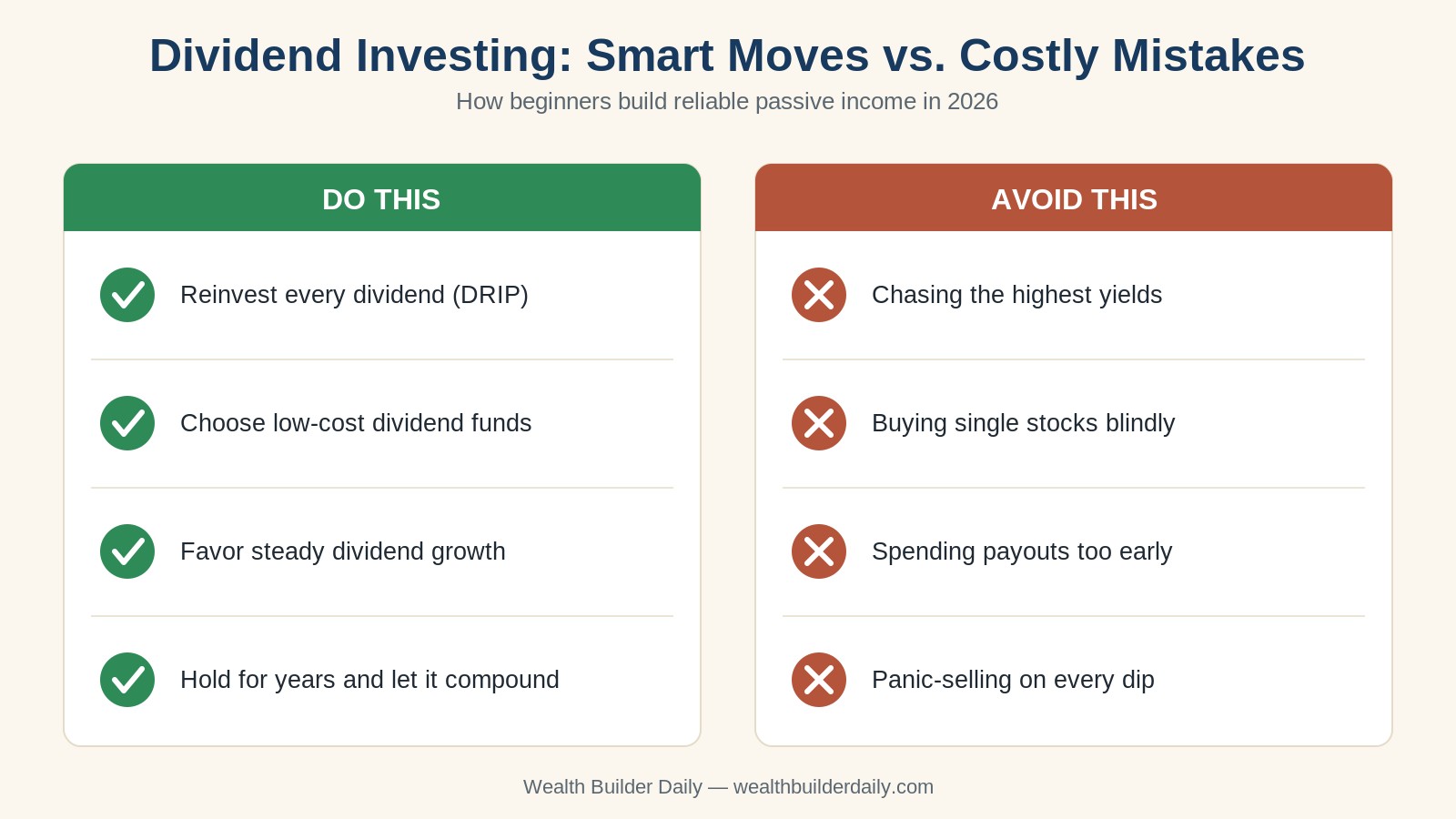

How to Choose the Right Dividend Investments

You don't need to pick the perfect stock. You need to pick a sensible mix and stick with it. Use these criteria to build your first dividend portfolio:

-

Start with a diversified fund. A low-cost dividend ETF spreads your money across hundreds of companies, so one bad quarter from a single business barely moves your income. This is the safest on-ramp for most beginners.

-

Look at dividend growth, not just yield. A company that has raised its payout for 25 straight years is often healthier than one with a flashy 8% yield. A high number can be a warning sign that the price has fallen for a reason.

-

Check the payout ratio. This is the share of profits a company pays out. A ratio under roughly 60% usually means the dividend has room to keep growing. A ratio near or above 100% can mean the payment is fragile.

-

Mind the fees. A fund charging 0.06% keeps more money in your pocket than one charging 0.60%. Over decades, that gap alone can be worth thousands.

-

Match the income to your goal. If you want growth now and income later, lean toward dividend-growth funds. If you want bigger checks today, you might add some higher-yield holdings with eyes open to the extra risk.

Here's an expert tip with real numbers: if you invest $300 a month into a dividend fund yielding 3% and growing its payout, and you reinvest everything, you could be looking at well over $120,000 in 20 years — with a meaningful slice of that coming from reinvested dividends alone. Before you start, make sure you've got an emergency fund in place so you're never forced to sell during a dip.

High Yield vs. Dividend Growth

New investors often ask whether to chase the biggest yield or the steadiest grower. High-yield stocks pay more cash today but can cut their payouts when business gets tough. Dividend-growth companies pay less now but tend to raise their payments year after year, which protects you against inflation. For most beginners in 2026, a growth-tilted approach with a few higher-yield holdings is the calmer, more reliable path.

Dividend Investing for Beginners in Every Situation

There's no single "right" way to invest in dividends — the best approach depends on where you are in life and what you want your money to do. The good news is that the same core habit, owning quality companies and reinvesting their payouts, works at every age. What changes is the balance between growth and income as you get closer to actually spending the money.

- The young builder (20s–30s): You have decades for compounding to work. Favor dividend-growth funds and reinvest everything. Pair this with broad index funds and ETFs for maximum long-term growth.

- The mid-career saver (40s–50s): Keep reinvesting, but start eyeing the income your portfolio could throw off later. A balanced mix of growth and yield fits well here.

- The near-retiree (60s+): Now those payments can become real spending money. A steadier, higher-yield tilt can help cover living costs without selling shares.

Beginner, Intermediate, and Advanced Setups

A beginner can do beautifully with one diversified dividend ETF inside a brokerage or retirement account. An intermediate investor might hold two or three funds to balance growth and income. An advanced investor may add individual Dividend Aristocrats or REITs for targeted income, while still keeping a low-cost fund as the core.

Personalizing Your Approach in 2026

The best portfolio is the one you'll actually stick with. In 2026, opening an account and turning on automatic investing takes about fifteen minutes. If you're not sure where to begin, our guide to opening your first brokerage account walks you through it step by step, and holding dividend funds inside a Roth IRA can let that income grow tax-free.

Frequently Asked Questions

How much money do I need to start dividend investing?

You can start with as little as $5 to $50 thanks to fractional shares offered by most brokerages in 2026. There's no minimum balance required to begin building income. The key isn't how much you start with — it's starting early and adding to it consistently, since every dollar you invest begins earning dividends right away.

Are dividends taxed differently than regular income?

Often, yes. "Qualified" dividends from most U.S. stocks held long enough are taxed at lower long-term capital-gains rates, while "ordinary" dividends are taxed like regular income. Holding dividend investments inside a Roth IRA or 401(k) can shelter that income from taxes entirely, which is why many beginners start there first.

Can I live off dividends one day?

It's possible, but it takes time and capital. To generate $40,000 a year at a 4% yield, you'd need roughly $1 million invested. That sounds huge, but consistent monthly investing plus decades of reinvested dividends can get many people there. The earlier you start in 2026, the more realistic that goal becomes.

Final Thoughts

Dividend investing for beginners isn't about picking the next hot stock — it's about owning good businesses, collecting your share of the profits, and letting reinvested payments compound quietly in the background. Start with one diversified fund, reinvest everything, and give it time. That's the same promise we opened with, and it holds up because it's how real wealth gets built.

Here's why thousands of everyday readers trust Wealth Builder Daily to guide their money:

- Plain-language guidance: We explain every term so you never feel lost or talked down to.

- Real numbers and examples: Our advice is grounded in actual dollar figures you can act on today.

- Proven, time-tested methods: We focus on strategies that have built wealth for decades, not fads.

- Free, practical tools and guides: Everything you need to take the next step is available at no cost.

The best time to plant a dividend tree was years ago. The second-best time is today — and 2026 is yours to start. Explore more beginner-friendly strategies on the Wealth Builder Daily blog, and when you're ready to dig deeper into the basics of investing safely, the SEC's free resource at Investor.gov is a trustworthy place to keep learning. Your future income stream starts with the first share you buy.

The Newsletter

Get the Free Budget Tracker

Join our weekly newsletter. Practical money guides, no fluff. Unsubscribe anytime.